There's a world of opportunities in commercial finance

Diversifying into commercial finance is a wise career move for brokers right now. The heat is dissipating from Australia’s real estate sector, with some analysts predicting house prices will fall by 20% or more by 2023 based on the Reserve Bank’s current trajectory of official cash rate hikes.

Rising interest rates and inflation have dampened buying and selling of property, but there is also intense competition between lenders and therefore brokers for the growing number of mortgage holders seeking to refinance their home loans to get a better rate.

Many residential brokers have clients who are self-employed or small business owners, and they have organised their home loans through these brokers, but not their business-related finance needs.

That’s an opportunity lost for brokers, who with the right education, training and support from lenders and aggregators could be tapping into a vast market by offering these clients commercial loans.

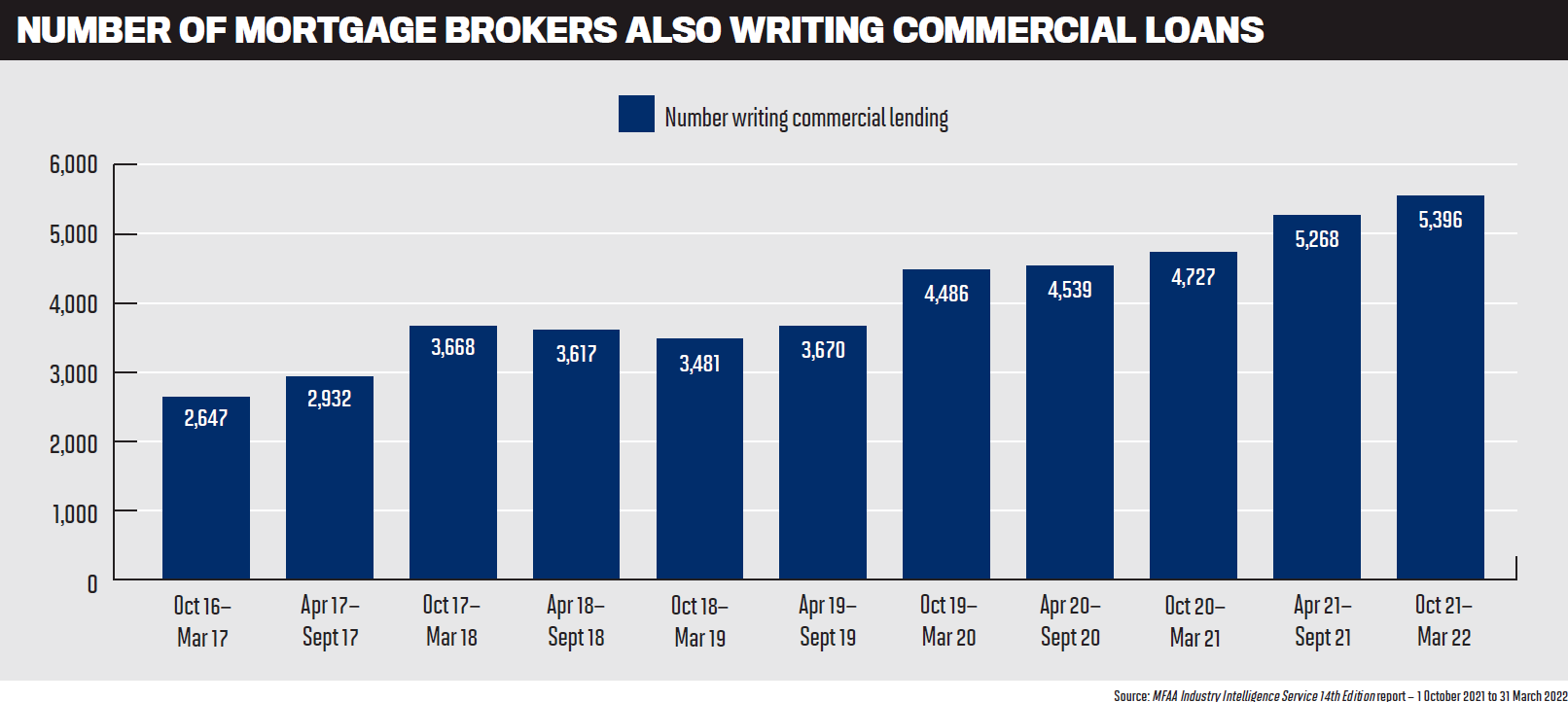

The latest figures from the MFAA’s Industry Intelligence Service 14th Edition report, covering 1 October 2021 to 31 March 2022, show that the proportion of mortgage brokers also writing commercial loans now stands at 29%, up 0.2% on the previous six months. Year-on-year this represents a 14.1% increase, or 669 more brokers writing commercial/asset finance loans.

The figures indicate that there’s huge scope for growth in the commercial lending sector – and certainly far less competition than for residential home loans. Diversifying into the commercial space can help brokers prevent clients from going elsewhere for business finance, strengthen client relationships and grow their businesses through word-of-mouth referrals.

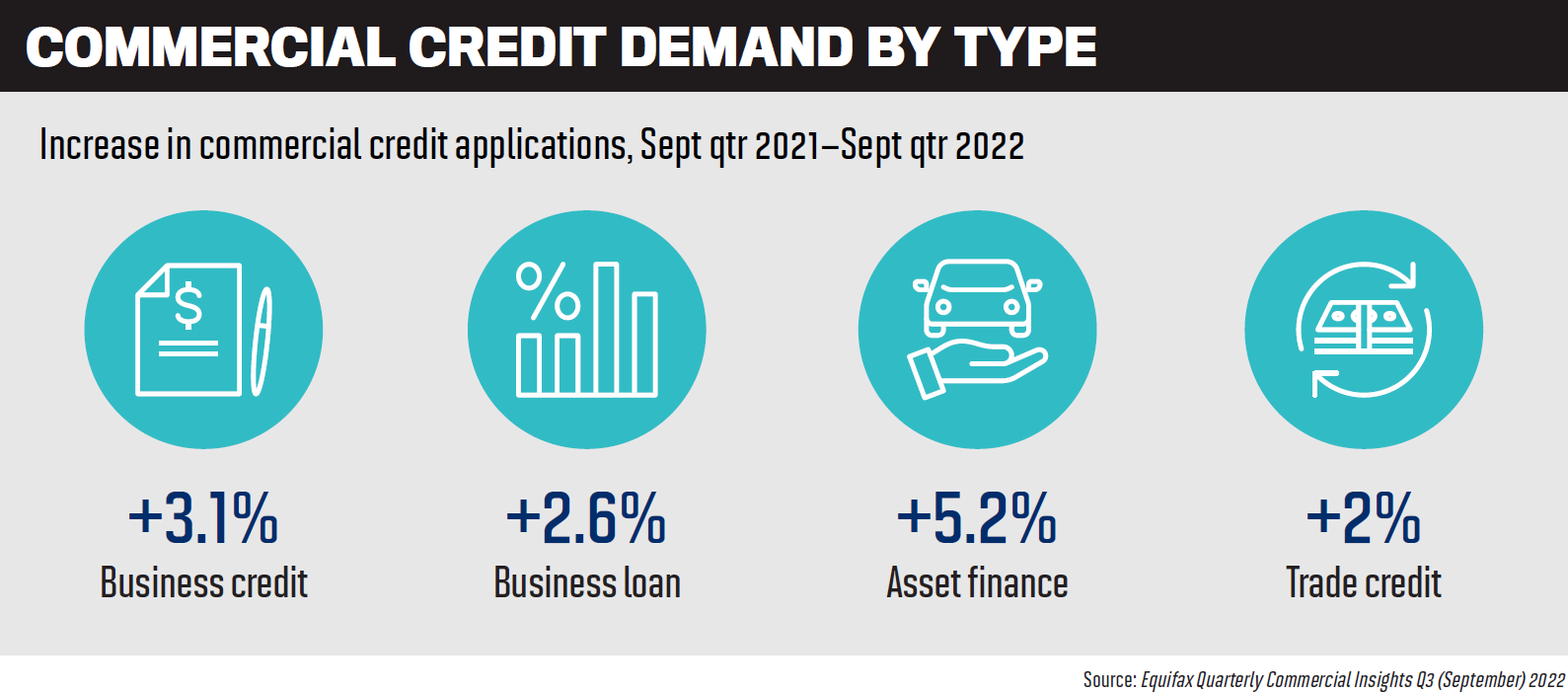

In a national economy dominated by small to medium-sized businesses – 98% of the 2.4 million businesses in Australia are SMEs – the recovery from the pandemic continues. Equifax’s September quarter Commercial Insights index shows demand for business loans, trade credit and asset finance has increased year-on-year. Business loan applications grew 2.6% in the September quarter compared to the same quarter in 2021 and a whopping 25.2% compared to 2020.

Non-bank lenders Thinktank, Prime Capital and OnDeck Australia, customer-owned bank Gateway Bank and major broker aggregator AFG have shared with MPA how they support broker diversification, and the benefits it provides. They say commercial finance is not as difficult or complex as some brokers assume.

Encouraging diversification

Despite the growing number of mortgage brokers dabbling in the commercial space, it’s just a drop in the ocean in terms of the size of the market. So, how can the industry encourage brokers to get on board?

Gateway Bank’s chief operating officer, Zeb Drummond (pictured below), says education, engagement and support are key to the growth of commercial lending in the broker market.

“Commercial is often perceived as too hard or complex and therefore too daunting to consider,” he says. “In reality, once the key principles are understood, just like in residential, it becomes very apparent when a deal is going to work and what lenders might be best.”

Peter Vala (pictured below), general manager partnerships and distribution at Thinktank, says that with rising interest rates, ongoing economic uncertainty, and competition between lenders, many borrowers are more actively considering their financial position.

“Some are looking beyond traditional residential loans to restructure debt and improve cash flow,” he says. “Others are taking a more aggressive approach in seizing on the market instability to expand their business operations and acquire commercial property. All of these activities are generating significant opportunities for brokers offering diversified solutions.”

Vala says brokers who have built strong and trusted relationships with their clients and can act quickly and flexibly when turned to for assistance, are the ones making the most of these opportunities.

David Drinkwater (pictured below), national sales manager commercial and asset finance at AFG, says the broker proposition is just as strong for SMEs as it is for residential customers.

“It makes perfect sense for brokers to be offering their SME customers commercial finance,” Drinkwater says. “Many SME customers have historically only dealt with the lender they hold their transactional banking with, and often there is no real face-to-face relationship with that lender. Customers have a relationship with their brokers, and brokers have proven to their customers the value they can add to the process.”

Drinkwater says brokers have a growing understanding of how great the opportunity to add commercial and asset finance to their proposition can be.

“The main barrier for brokers to offering commercial finance is around the time and willingness to invest in either people or training to gain the skills required to write commercial.

“We’re now seeing lenders, and aggregators like AFG, investing and bolstering resources for their commercial broker models that include more BDMs, streamlined training, and technology platforms that simplify commercial and asset finance broking.”

Prime Capital CEO Steve Sampson (pictured below) says providing education and improving skill sets is the key to encouraging more brokers to write commercial loans.

“Aggregators and lenders should be paving the way with programs to help brokers increase their knowledge and help them diversify,” he says.

“This becomes a win, win, win for all parties. Many brokers think that commercial lending and asset lending is complicated. Well, that depends on whom they deal with, and starting with more vanilla-type lending is the key to growth and success.”

Sampson says Prime Capital knows that for most residential mortgage brokers, 30% of their client bases are self-employed. “Through our knowledge and coaching webinars and learning sessions, we help them realise that untapped potential.”

OnDeck Australia CEO Cameron Poolman (pictured below) says increasing interest in commercial lending comes as no surprise to the lender.

“Our recent research confirms a high level of demand for brokers’ service across Australia’s small business community,” he says. “Our survey found six out of 10 small businesses (60%) would consider using a broker for their future financing needs. Moreover, an overwhelming 86% of small businesses would return to their broker for support with organising finance in the future.”

Poolman says the small businesses OnDeck surveyed cited a number of drivers for SMEs seeking a broker’s support, including:

- 59% want the advice and opinion of a broker

- 45% have found a broker helpful in the past

- 41% want the best price possible for finance

- 31% lack time to independently arrange financing

- 12% require finance urgently

“The key is for brokers to realise the breadth of opportunity that small business lending offers,” Poolman says. “The challenge facing brokers is that small business lending is traditionally a much-neglected area across the big banks, and small enterprises can experience a high rate of rejection among traditional lenders.”

OnDeck research in 2020 found that of small businesses that had applied for finance in the past, one in four (24%) had been rejected by a bank when seeking a business loan.

But this “lack of attention” to small business lending among the big banks is creating exceptional opportunities for brokers, says Poolman. “They can step in and help their clients enjoy the benefits of a fast and efficient application and approval process offered by a dedicated small business lender that under-stands their needs.”

Moving away from property

Sampson says it’s inarguable that the residential market has slowed down, and some banks have publicly stated that they are not looking at growing their market share in this sector.

“That makes sense for them because the intense competition they have created over the last few years has stripped margins to a thread. If they aren’t growing, then neither will brokers, so there’s an imminent need to diversify,” he says.

“What we have is a perfect storm, rising interest rates and a subsiding residential property market. Investors are scarce, but commercial assets such as industrial proper ties are holding strong. If a broker wants to grow their book, then probably the residential market is not the place.”

Drinkwater says right now there’s a substantial uplift in the number of brokers interested in offering commercial finance, compared to the past two years.

“There is a genuine window of opportunity for brokers to make a tactical diversification that can open new revenue streams and add substantial value to their loan books. With over 100 commercial and asset finance lenders in the market, customers can find themselves confused, bewildered and in need of a broker to help them find the right product for their needs,” he says.

Poolman says a slowdown in the residential property space was inevitable to a degree, given the cyclical nature of the market, and this will impact brokers who focus solely on residential lending.

OnDeck has seen significant growth in small business lending volumes since the end of pandemic lockdowns when businesses were able to take advantage of pent-up consumer demand. The non-bank lender recorded 43% growth in loan originations in the first six months of 2022, following the company’s management buyout by an Australian team in late 2021.

“We are seeing brokers diversify into commercial lending because they recognise that fintech lenders such as OnDeck are meeting the needs of their small business clients with an application process that is fast, efficient and easy to navigate,” says Poolman.

This is important as small businesses can’t afford a protracted application and approval process, he says. “OnDeck uses a technology-based approach that allows brokers to get the deal done sooner.”

This includes requiring just six months of bank statements to be uploaded to OnDeck’s secure portal for loan applications, while its Lightning Loans can be assessed in as fast as one hour.

“We believe this is the fastest in the industry, and it benefits the broker and the small business,” says Poolman.

Vala says over the past few years the residential mortgage space has been exceptionally busy, and many brokers either didn’t see the need or perhaps didn’t have the time to look at diversifying.

“With lending opportunities now slowing in pace, many brokers are taking the opportunity to upskill and strengthen their businesses, while adding new income streams in the process,” he says.

“This may include expanding their offering into areas such as commercial property, SMSF lending and asset finance. The key is for a broker to review their book of clients and see what new product and finance offerings can reasonably meet their needs now and in the future – and then plan for that.”

Drummond says the slowdown of new sales in residential, with changing consumer behaviour, is impacting brokers and will continue to do so.

“We may go some time before we see the rates of purchase activity growth that we have seen in recent years,” says Drummond.

“The focus will shift to refinances and to servicing existing clients more broadly. Commercial lending is a great way for a broker to open up new customer segments, diversify their loan book and expand the income opportunity.”

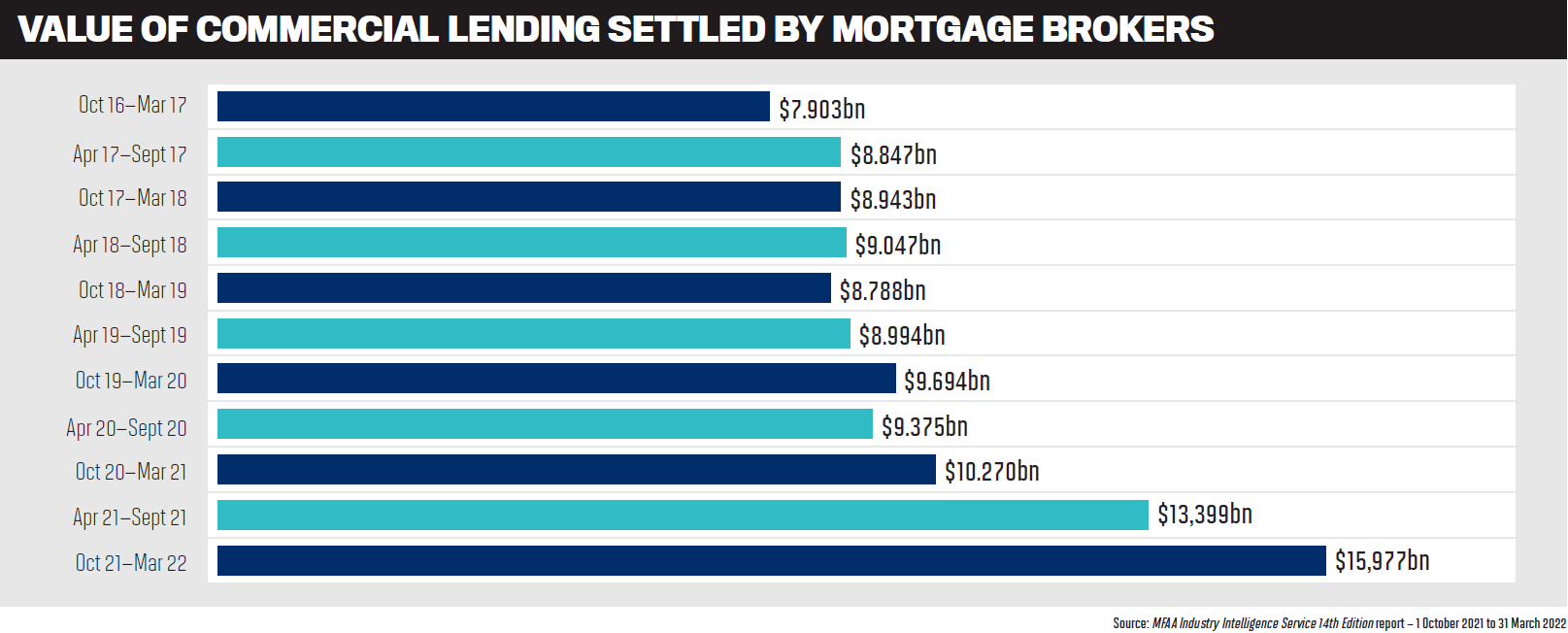

Drummond says the MFAA Industry Intelligence Service report for the six months to 31 March 2022 shows that the number of brokers diversifying and leveraging this opportunity has increased drastically, leading to a $5.7bn rise in commercial loans written year-on-year. “That’s a lot of loans,” he says.

Offers of training and support

Drinkwater says AFG has set up an entire division dedicated to commercial and asset finance. It was specifically created to help brokers start doing commercial finance.

He says after helping hundreds of residential brokers diversify into commercial finance, AFG developed a framework that focuses on three key aspects of the support it provides:

- Highly focused training that is accessible digitally as well as in person and covers everything from the basics through to the nuances of structuring commercial deals

- Simplified technology that assists with lender selection, information collection, submissions and accreditations

- An army of commercial experts, including local BDMs and a national scenario and support desk for working hand in hand with brokers to structure deals

Poolman says, “Brokers who are uncertain about commercial lending can rest assured that OnDeck’s accreditation process is very straightforward, and our experienced team of BDMs is available to offer support at every stage.”

He says OnDeck’s technology-driven approach makes loan applications easy: after uploading six months of bank statements to the secure OnDeck portal, the bespoke KOALA Score™ credit assessment algorithm drives a turbo-charged funding decision.

Poolman says OnDeck has invested in promoting its free ‘Know Your Score’ tool to the broking community. “It allows brokers to have conversations with their small business clients around the credit score of the busi-ness. One in two small businesses aren’t even aware that a business has its own credit score independent of owners, so this can be a great way for brokers to engage and educate their small business clients.”

Drummond describes Gateway as a small lender, “not an industrialised machine”.

“We use technology to help us move quickly through the mundane, but appreciate the value in workshopping a deal and connecting brokers with good bankers,” he says.

Gateway entered the market with a simple product with a simple headline rate to help overcome the complexity barrier for both brokers and their clients.

“We wanted to make the process as trans-parent as possible with our brokers and didn’t feel like risk-loaded below-the-line pricing was helpful in that regard,” says Drummond. “This is also why we opted to have a product that didn’t require annual reviews, as these can increase the broker and banker low-value administrative burden.”

Benefits of new market trends

Vala says one of the clear trends at present is the increase in refinancing as borrowers look for ways to improve their surplus cash flow via consolidating debt or extending loan terms.

“This need to optimise finances has also resulted in SMSF purchases and refinances remaining strong, with borrowers seeking to utilise the most beneficial tax structure possible to support their retirement expectations,” he says.

In terms of growth areas, Vala says the high demand for industrial property is resulting in a substantial increase in transactions and opportunities in this sector. “In fact, our latest market report has highlighted industrial as the only market segment in Australia that’s improving in every capital city.”

With the demand for residential finance continuing to decline, diversification can offer significant benefits, says Vala. “Primarily, it’s a valuable strategy for brokers in deepening existing relationships as borrowers seek alternative lending options, which in turn grows business. It really comes down to having the implicit flexibility to meet a client’s varying finance needs.”

Vala says the more product solutions a broker can deliver, the greater chance they will have of retaining existing clients and opening up new opportunities. “Brokers who are skilled up to diversify into areas such as commercial and adapt to the challenges of a fluctuating market will be ideally placed to strengthen their business and prosper.”

Sampson says fast and simple loans are the key: “We believe this so much that we have trademarked the term.”

“SMEs don’t have time to waste when they require finance,” he says. “Forty-three per cent of SME borrowers say the main challenges they experience are that lender requirements are strict; and the amount of time the process takes. Brokers using the right lenders that understand these requirements can carve out a niche for themselves and do it quickly.”

Drummond says there are many customers that have existing commercial loan facilities.

“Commercial customers behave in a different fashion to residential borrowers as they have different needs,” he says. “Commercial lenders behave in a slightly different way too; shorter-term facilities are commonplace due to how commercial facilities are and have been written. This presents as an opportunity to write a large number of deals quickly as review periods drive borrower behaviour.”

There are two main areas of commercial lending that have seen significant growth, says Drinkwater: products that don’t require full accountant-prepared financial data (lease-doc, low-doc, accountant declaration); and SMSF lending.

“In particular, SMSF lending creates a great opportunity for brokers, as a number of the major trading banks pulled out of this market due to the perceived complexity of the transactions,” he says.

“Providing a holistic service offering to your SME customers will assist in customer retention,” he adds. “And apart from the additional income stream, it also adds value to your potential trail book multiplier should you wish to sell.”

The question of qualifications

It may come as a surprise to some residential brokers, but extra qualifications are not required to become a commercial broker, although it’s a good idea for brokers to seek the support of their aggregators and lenders when taking on commercial loans.

Vala says there are no minimum education, experience or volume requirements for workshopping and submitting a loan application to Thinktank. “Our entire focus is to quickly and effectively equip brokers to expand their networks into areas such as commercial and SMSF lending, including how best to structure loan applications and secure a timely approval. To support this, our team of dedicated relation-ship managers are there to help brokers, from establishing the loan through to settlement.”

While no additional qualifications are needed to become a commercial broker, Drinkwater says some lenders want to ensure the broker is either active in this space, completes appropriate training, and/or is a member of a commercial lending industry body.

“AFG’s business program has a conversion ratio of 70% from lodgement to lender to settlement,” he says. “This is based predominantly on the lender-matching capability and knowledge of the lender’s information requirements once a product is chosen.”

Sampson says for brokers to submit commercial loan applications to Prime Capital, the standard industry qualifications for writing residential loans are needed, along with Prime Capital’s accreditation training.

Drummond says while the standard industry qualifications are the same, where the gap lies is in education. “Gateway has different accreditation content that brokers complete before being able to submit a commercial application. The content specifically covers the commercial product range and process for submission.”

The value of mentors

Drummond says there are face-to-face and remote courses that can help brokers with the theory and practice of writing commercial loans, “but nothing really beats sitting down with someone to workshop a deal”.

“A mentor is critical to success in this regard,” he says. “Our commercial bankers are also set up to support brokers workshopping deals – this is something we wanted to contribute to the industry.”

Sampson says the need for brokers to have a mentor depends on the complexity of the applications that the broker chooses to work with. “Most aggregators and lenders have excellent support to assist their introducers.”

Drinkwater agrees that there are some complexities in moving into commercial. “Scenarios sometimes come with unique characteristics whereby there will be great benefit in having an experienced mentor or good technology that can assist in narrowing lending options and structuring the transaction. AFG provides a unique proposition whereby we offer both technology, BDM support and a lending scenario support desk via our business program.”

Vala says a trusted mentor who brokers can turn to is a great advantage when diversifying into commercial property, particularly as the sector covers a wide spectrum of lending.

“It’s advisable that a broker has more than one mentor or subject matter expert they can turn to in order to support all their commercial lending and knowledge needs,” he says.

“Our best piece of advice for brokers is to ask lots of questions and gather as much intel as possible with any new transaction. Have two or three trusted RM or BDM lenders with different lending backgrounds who can work-shop transactions and recommend the best path to follow.”