With plummeting affordability, the NSW government has recommended cutting capital gains tax in a bid to make homeownership more achievable

Everyone has been watching property market prices continue to rise and affordability drop. Although the monthly rate of growth in Australian dwelling values recorded by CoreLogic has slowed, it is still increasing at around 1.5% per month. At their peak in March 2021, dwelling prices rose by 2.76% that month. Not surprisingly, Sydney was most affected, reporting a peak growth rate of 3.7%.

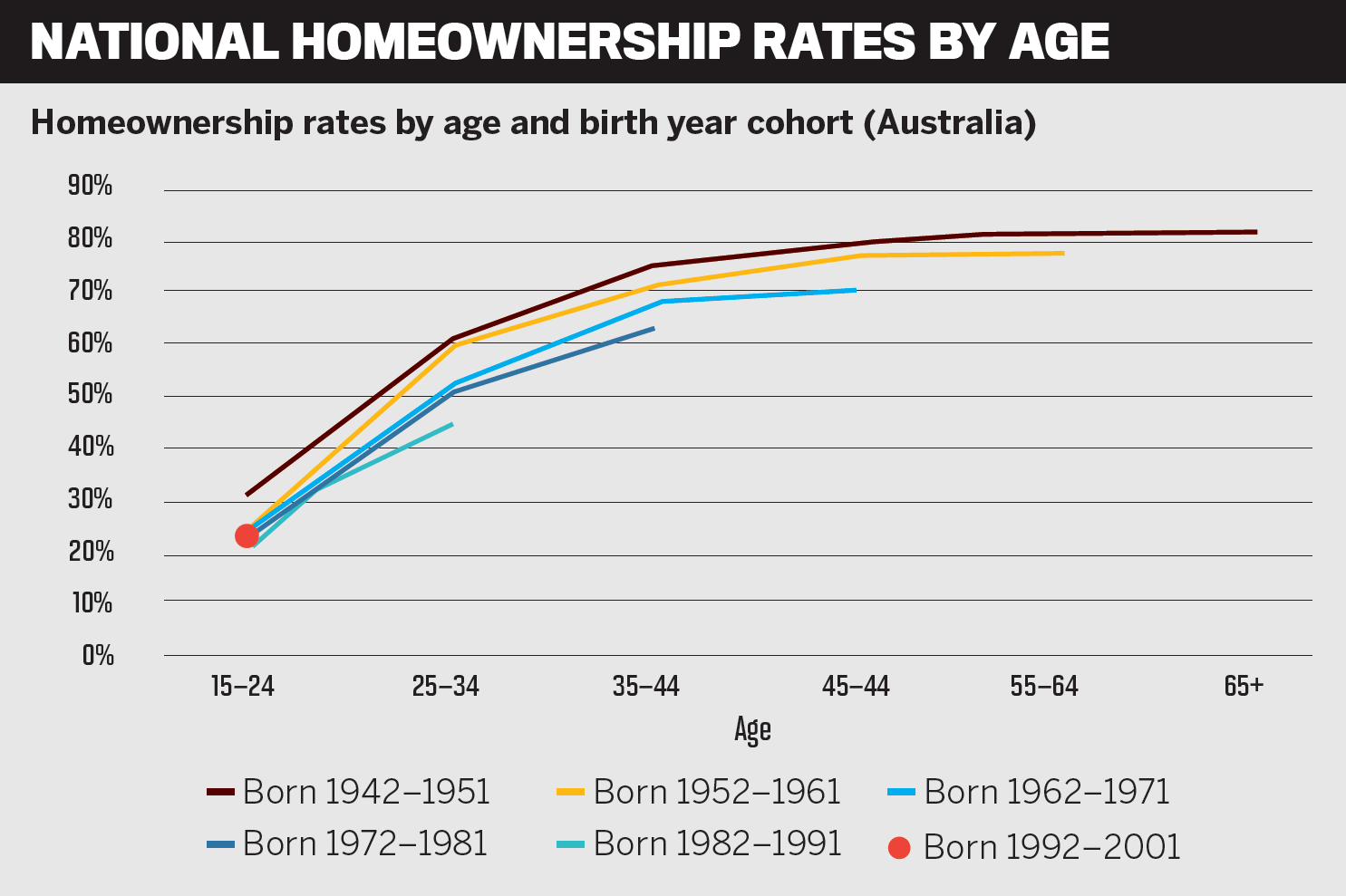

According to the NSW Intergenerational Report released earlier this year, the rate of homeownership is being affected too. The share of people who owned a home in NSW peaked at 70% in 1966. In the 50 years since then, the homeownership rate in NSW and Australia remained relatively stable, but over the past decade it has started to decline. In the 2016 Census, it was the lowest it had been since 1954. The NSW Intergenerational Report said the outlook for homeownership rates was uncertain.

To tackle the falling homeownership numbers, in August the federal government announced an inquiry into housing affordability and supply in Australia. As part of its call for submissions, hundreds of organisations sent in documents with their recommendations.

One of these submissions came from the NSW government, which recommended that the Commonwealth Government provide incentives and remove disincentives to states and territories for “undertaking major productivity-enhancing taxation reforms” – for example, removing stamp duties.

It also recommended cutting the capital gains tax concession, arguing that it was leading to significant purchases of properties for investment rather than accommodation.

“The NSW Government has proposed a new Property Tax Reform that seeks to transition from the current stamp duty and land tax system to a broad-based annual property tax based on unimproved land values,” the submission said.

“The NSW Government aims to make home ownership more achievable by proposing to address the upfront barrier of stamp duty and help people live where they would like to suit their stage of life. This proposal should make housing more affordable for all people.”

The belief that capital gains tax concessions could help is not held across the board, however. Arjun Paliwal, founder and head of research at InvestorKit, said it could actually drive greater price rises.

He pointed to ABS lending figures which show that, pre-COVID-19, new loan commitments to investors were declining, and throughout the pandemic they have not risen substantially.

“These numbers suggest tax breaks such as the capital gains 50% exemptions do very little to create investor speculation,” Paliwal said. “Removing this will only create greater supply constraints, as investors will hold on to assets for longer to create gains worth of selling if this tax is removed. In turn, it can create greater price rises, the opposite of what the thought on this policy is.”

Speaking at a public hearing of the inquiry, Customer Owned Banking Association CEO Michael Lawrence said that now was the time to bring a new commitment to tackling the problem across all levels of government. Noting that first home buyers were finding it increasingly difficult to save enough money to buy a home, Lawrence said housing prices were now at a ratio of six times typical household disposable income – up from 2.5 times 30 years ago.

He said adding stamp duty to a house price often increased the time it took to save a 20% deposit by two and a half years, assuming the potential borrower was working full-time on average earnings and saving 15% of their income.

“We have a quote in our submission from the RBA Governor about house prices reflecting the value of land, which is driven by factors such as urban design, planning laws, transportation and taxation. These factors, along with others such as immigration, drive housing supply and demand and therefore housing affordability, and collectively fall within the remit of all levels of government,” Lawrence said.

“A collective problem needs a collective solution. The biggest lever governments have to improve housing affordability is to boost supply.”

In a survey of Australian consumers run by Canstar, around three in 10 people said banks and lenders should increase home loan interest rates to help cool the property market.

Of the 22% who believed increasing interest rates was not the right move, 27% said negative gearing and capital gains tax should be scrapped.

Other respondents suggested that first home buyers should receive extra support to compensate for price increases (36%); there should be tougher restrictions on investors (33%); and there should be less red tape (29%), which would encourage property development and construction, adding to the supply of housing.

Canstar’s group executive financial services, Steve Mickenbecker, warned that there was increasing pressure to increase interest rates, but this could spell trouble for some existing homeowners.

“Just over half of Australian adults believe the property market needs cooling, but it may be a case of ‘be careful what you wish for’ for the almost one in three Australians who would welcome interest rate increases, as the pursuant mortgage stress would be quite a drag on the economy beyond housing prices,” Mickenbecker said.