The Family Home Guarantee scheme is designed to help single parents achieve their homeownership dreams sooner. Find out if you're eligible in this guide

Single parents often bear the responsibility of sole caretaker and income earner. This makes owning a home harder, especially with house prices continuing to soar.

A recently introduced government-backed scheme has made homeownership more attainable for single-parent households.

The Family Home Guarantee (FHG) aims to help single parents and legal guardians buy a home faster. Find out how this housing initiative works and if you’re eligible in this guide.

What is the Family Home Guarantee?

The Family Home Guarantee is a government initiative designed to help single parents and legal guardians with at least one dependant purchase a home sooner. It is administered by Housing Australia under the Home Guarantee Scheme (HGS).

Under the FHG, the government guarantees a portion of the home loan. This allows single parents and legal guardians to buy a home with as little as a 2% deposit, without having to pay lenders’ mortgage insurance (LMI).

The Family Home Guarantee was introduced on 1 July 2021. It will run until 30 June 2025. Initially, 10,000 places were made available for the four-year period or 2,500 for each financial year. The number increased to 5,000 places a year during the Federal Budget in 2022.

Who is eligible for the Family Home Guarantee?

The Family Home Guarantee was initially designed for single parents with at least one dependant. The government extended eligibility to single legal guardians on 01 July 2023. These include aunts, uncles, and grandparents. The scheme is open to both existing homeowners and first-time home buyers.

To qualify for the FHG, you must be:

- a single parent or legal guardian of at least one dependant

- applying as an individual

- an Australian citizen or permanent resident

- at least 18 years old

- have a taxable income not exceeding $125,000 per annum for the previous financial year (child support payments excluded)

- not have any ownership interest in other properties at the time of application

You’re not considered single if you’re separated from your spouse but not yet divorced. If you’re not married but are in a de facto relationship, you’re not considered single either.

What types of properties are eligible for the FHG?

The Family Home Guarantee can be used to build a new house or buy an existing property. You must be the owner-occupier of the home, meaning you intend to live there.

Here’s a list of eligible properties under the scheme:

- an existing house, townhouse, or apartment

- a house and land package

- land and a separate contract to build a home

- an off-the-plan apartment or townhouse

All properties must be residential. Investment properties aren’t covered by the FHG.

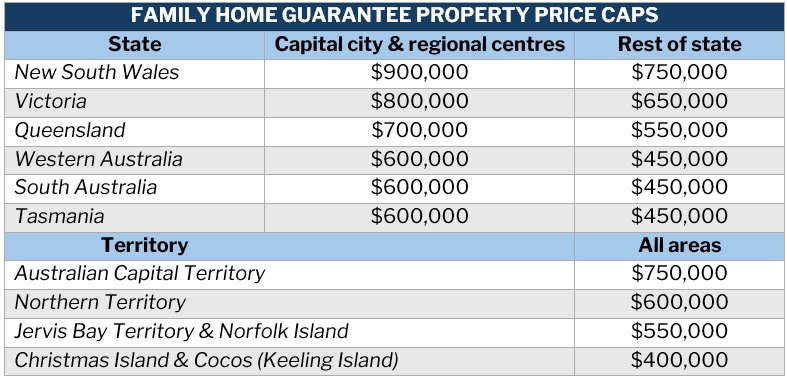

Each state and territory has a price cap for eligible properties. If the home you’re planning to buy exceeds these thresholds, you cannot apply for the Family Home Guarantee.

In New South Wales, regional centres only include Illawarra, Newcastle, and Lake Macquarie. In Victoria, these cover only Geelong, while in Queensland, only Gold Coast and Sunshine Coast are included.

How can you apply for the Family Home Guarantee?

If you’re an eligible single parent or legal guardian and your home choice qualifies, you can only apply for the Family Home Guarantee through a participating lender.

There are 36 lenders participating in the FHG. Six of these are major banks. You can choose from any of the lenders below. Click on the links to find out how you can apply. You can also get information on how your home loan can be covered by the Family Home Guarantee through these lenders.

Family Home Guarantee – Participating lenders

|

Major lenders |

||

|

Non-major lenders |

||

Housing Australia doesn’t accept applications for the Family Home Guarantee. It also doesn’t maintain a waiting list. Applications for the FHG are free of charge. If approved, however, you’re required to meet all costs and repayments for the home loan guaranteed under the scheme.

The Family Home Guarantee (FHG) shouldn't be confused with the First Home Guarantee (FHBG), which is designed only for first-time home buyers. You can learn more about the FHG in this information guide.

How does the 2% deposit scheme work?

Any guarantee of your home loan under the FHG is capped at 18% of the property’s value as assessed by your lender. This means that you can contribute at least 2% deposit to make up the required 20%.

The guarantee, however, isn’t a cash payment or a deposit for your home loan. Instead, it is a legal arrangement between Housing Australia and your lender. Under the agreement, Housing Australia will pay the lender what you owe if you default on your mortgage and the home has been sold.

The Family Home Guarantee requires that you use the full amount of your savings for your deposit. If you already saved at least 20% for the deposit, then your home loan cannot be covered.

The FHG is intended to help single parents and legal guardians who are struggling to save for a deposit. It’s important not to game the system by changing your circumstances just to take advantage of the scheme. This includes legally transferring your money to hide the true amount of your savings or having the 2% deposit given to you just to qualify.

If you’re not eligible for the Family Home Guarantee, there are several other government-sponsored benefits that can help you achieve your homeownership dreams. Check out this guide on home loans for first time buyers in Australia to find out which schemes you qualify.

Do you think the Family Home Guarantee provides single parents with a faster way to buy their dream homes? Is the support Housing Australia offers enough? Share your thoughts in the comments below.