Mortgage transfer allows you to carry over your loan from your current home to a new one. But how does it work exactly? Read on and find out

- But first, is your mortgage transferable?

- What is mortgage transfer?

- How does a mortgage transfer work?

- Can you transfer your mortgage to another person?

- Who is eligible for a mortgage transfer?

- How can you transfer your mortgage to another property?

- What are the benefits and drawbacks of mortgage transfer?

- Do you have to stay with the same lender?

Updated 20 March 2024

Because most Australians do not stay in the same home for more than 15 years, it is a good idea to know about mortgage transfer. Also known as loan portability, this feature allows you to simply transfer your mortgage from one address to another with minimal headaches.

If you are happy with your home loan and want to take it with you when you buy a new house, this guide can prove useful. Read on and find out how mortgage transfer works and if it is right for you.

But first, is your mortgage transferable?

The short answer is: Yes, your mortgage is transferable. When you take out a mortgage, you enter a commitment that usually lasts for decades. If, during that period, you decide to move onto a new property, most banks and lenders will allow you to transfer your mortgage. This feature is popularly known as loan portability.

The loan portability feature allows you to sell your current property and buy a new one while retaining the original mortgage.

Considering most Australians seldom stay in one home for more than 15 years, the loan portability feature is especially helpful.

Typically, people move homes before the loan term ends. You may do so to save time on daily commutes, accommodate growing families, or simply to get a change of scenery. Regardless of the reasoning, you can have the common option to transfer your mortgage.

What is mortgage transfer?

Mortgage transfer lets you transfer your home loan to another property without the need to apply for a new one. This means that the interest rate, balance, and other built-in features of the loan are carried over to the new property. When the mortgage transfer is finished, your mortgage will be secured against your new home rather than the old one.

A mortgage transfer is used because it can free you from the complex process of yet another home loan application, also called refinancing. Mortgage transfer also allows you to retain the features that come with your current mortgage, such as your offset account.

Let’s say you have a home loan of $600,000 on a property that costs $780,000. You are also on the third year of the initial 30-year loan term, meaning there are 27 years left.

After the selling costs and real estate agent commission, you earn $750,000 after selling the home for $780,000. Instead of paying your home loan and applying for a new mortgage, you transfer that loan to your new home, which now costs $800,000.

Between your savings account and the $150,000 profit you made on your first home, you have the money to cover the $200,000 shortfall between the $800,000 purchase price and the $600,000 loan value.

How does a mortgage transfer work?

A mortgage transfer works similarly to how you transfer bills, such as your electricity and internet bills, to your new address when you move. The main difference is that your address changes, but the terms of your policies stay the same.

While it requires quite a lot more than a simple phone call, a mortgage transfer works in a similar way.

The process of a mortgage transfer will vary depending on which lender you use. In most cases, however, you will be required to:

- ask for a property form

- organise to have your initial home and your new home valued

- give a contract of sale on your initial home and your new home

A mortgage transfer is usually convenient and can save you cash because you do not need to apply for a new loan. This helps you avoid paying establishment and application fees.

You are also not required to change your loan numbers and direct debits. In addition, your home loan continues its original path. This means that if you are six years into a 30-year term, your loan moves with you to your new home, and you still have 24 years left until you own your property in full.

Simultaneous settlement vs. deferred settlement

Another factor to consider during mortgage transfer is the settlement date. Lenders often require that the home you are selling and the one you are buying have the same settlement dates. This arrangement is also referred to as simultaneous settlement.

Same date settlement makes the process easier for the lenders as they can simply substitute one property for the other as security for the mortgage. Making this happen, however, can sometimes be challenging.

To arrange for simultaneous settlement, you will need to negotiate with both the buyer of your home and the seller of the new property to make sure that the dates line up.

If this is not possible, your other option is a deferred settlement. You can negotiate for this arrangement if you have already sold your house but have not yet bought a new one. This means your home loan is still in place but there is no property securing it.

When this happens, some lenders will allow you to set up a term deposit as security against the home loan. You will still be required to meet mortgage repayments.

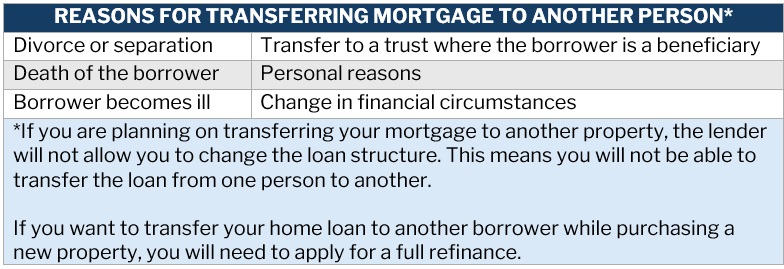

Can you transfer your mortgage to another person?

If you have an outstanding mortgage, it may be possible to transfer it to another person, but this will involve a different process.

To meet responsible lending laws, your lender must go through the usual application process to ensure that the other person meets its eligibility and serviceability criteria. Only then can the lender approve or reject the transfer.

Your lender will likely require a refinance. This means you will need to pay out the existing home loan and take out a new mortgage under the other borrower’s name.

Who is eligible for a mortgage transfer?

Before you can transfer your mortgage to a new property, you will need to meet your lender’s mortgage transfer requirements. Banks and lenders use different criteria regarding who is eligible but generally they consider the following factors:

The home’s value

Lenders often require a like-for-like substitution. This means that the value of the new property must be equal or greater than that of your current home. There are also instances where lenders allow a new home of lesser value, for example, if you’re downsizing. This will depend on how much equity you’ve built, your outstanding balance, and the new home’s valuation.

The property’s size

Most lenders require homes to be at least 40 square metres. Properties smaller than this are often seen as too risky.

The property title

The title of the new property must bear the name of the borrower or guarantor whose name appears on the loan contract.

Your repayment history

You will need a clean history showing timely repayments to be approved for a mortgage transfer.

How can you transfer your mortgage to another property?

One of the benefits of loan portability is that it enables you to transfer your mortgage to another property without going through the complex process of refinancing. Mortgage transfer takes a few simple steps:

1. Talk to your lender or mortgage broker

To get the process underway, you will need to inform your lender or broker of your plan to transfer your mortgage. You can do this as soon as you spot the new home that you like.

2. Get your paperwork ready

Because you will not be going through the entire home loan application process, this also means less documents needed. You must show proof that you are moving places such as the contract of sale and contract of purchase. You will also need to provide valuation documents for the new property.

3. Arrange extra financing

You will need this if the new property is more expensive than your current home. You can talk to your lender about your additional financing options.

What are the benefits and drawbacks of mortgage transfer?

Like any home loan feature, mortgage transfer comes with its share of pros and cons. It is important to know what they are and match them to your financial situation and your long-term plans.

Pros of mortgage transfer

Saving money on establishment fees: You can avoid this type of fee, which can range from $500 to $1,000, by transferring your old loan to the new property.

Avoiding exit fees: By doing a mortgage transfer you avoid paying exit fees. The amount varies depending on the lender but always includes a government fee of at least $197.

Saving time: You will not have to undergo the stress that comes with applying for a brand-new loan.

Cons of mortgage transfer

Restrictions: There may be restrictions when doing a mortgage transfer, such as changing the loan structure from fixed to variable. The interest rate and the number of borrowers may also be restricted.

Loan portability fee: While you could save in other fees, most lenders charge you a couple hundred dollars to transfer the loan.

Opportunity cost: The savings of exit and application fees may pale in comparison to a home loan cashback offer or refinancing to a loan with a lower interest rate.

Do you have to stay with the same lender?

Because mortgage transfer doesn’t allow changes in the loan structure, you are also required to stay with the same lender. This way, you can keep all the features of your loan, including offset accounts and redraw facilities.

That said, in a competitive lending market, there is an opportunity to find a lender that offers a better deal. Another way to make the most out of your home loan is to keep abreast of the latest industry developments. You can do so by subscribing to our free e-newsletters. Here, we will bring you breaking news and the latest industry updates that can impact your mortgage.

Do you think mortgage transfer is a good way to buy a new home? Have you experienced transferring your mortgage to another property? How was it? Feel free to share your thoughts in the comments.