Brokers have a vital role to play

Tight economic conditions and increased interest rates prompt savvy borrowers to shop around for the best home loans on the market with brokers playing a key role in their success.

Analysis from financial comparison site Mozo shows borrowers could save tens of thousands of dollars by comparing even the lowest of interest rates, and double checking their LVR tier.

However, Pepper Money general manager mortgages and commercial Barry Saoud (pictured above, left) said it’s important to remember there’s more to securing the correct loan than comparing rates.

“Brokers are playing a material role in helping borrowers to navigate the changing lending landscape and the demand for more flexible non-conforming options will continue to rise,” Saoud said.

“It’s important for brokers to empower and educate their clients to avoid making decisions based on the interest rate regimes.

“While the interest rate is an important consideration, the borrowers’ eligibility for credit and maximum borrowing capacity with a lender is key.”

High interest rates may persist

Mozo’s money expert Rachel Wastell (pictured above, right) said Australians need to get used to a higher-for-longer interest rate environment, following the last rise in November, and there is no way of predicting when this will end, or if it will.

“The RBA may start cutting the cash rate later this year, but it’s unlikely we’ll get back to those ultra-low interest rates starting with 1 or 2 we saw during COVID in the near future. In fact, they may never return at all,” Wastell said.

“It looks like inflation is heading in the right direction, but if you look at the rising cost of services like energy, insurance and housing, these are all still sitting well above the RBA’s target range of 2 to 3%.

“Further, if you consider the fact that monetary policy operates at a lag, the full impact of the 13 rate rises is only starting to flow through the economy now.”

Borrowers need to shop around

Wastell said borrowers need to get used to this higher-for-longer interest rate environment, and selecting the right lender is key.

“Home loans are six or seven figures of debt, which makes mortgages valuable commodities to the banks,” Wastell said.

“If you’re a mortgage holder that pays your mortgage on time and can meet serviceability requirements, you should remember that you hold a certain level of bargaining power.”

Wastell said the Australian home loan market is very competitive and, according to the Mozo database there are currently: 25 lenders offering rates starting with 5; 85 lenders offering rates starting with 6; 62 lenders offering rates starting with 7; and 39 lenders offering rates over 8%.

“When as little as half a percentage point difference in home loan rates can equate to tens of thousands of dollars more in interest you’re paying over the course of the loan, paying the ‘loyalty tax’ on a home loan can be very expensive,” Wastell said.

“When you look at the 0.10% difference in rates between the two lowest rate home loans on the Mozo database, you can see that 10 basis points equates to an extra $11,000 difference in interest paid over 25 years.

“Decimal points can be deceiving in home loans. So, if you can’t refinance due to serviceability, negotiating as little as a 0.10% drop in your rate with your current lender could save you tens of thousands of dollars.”

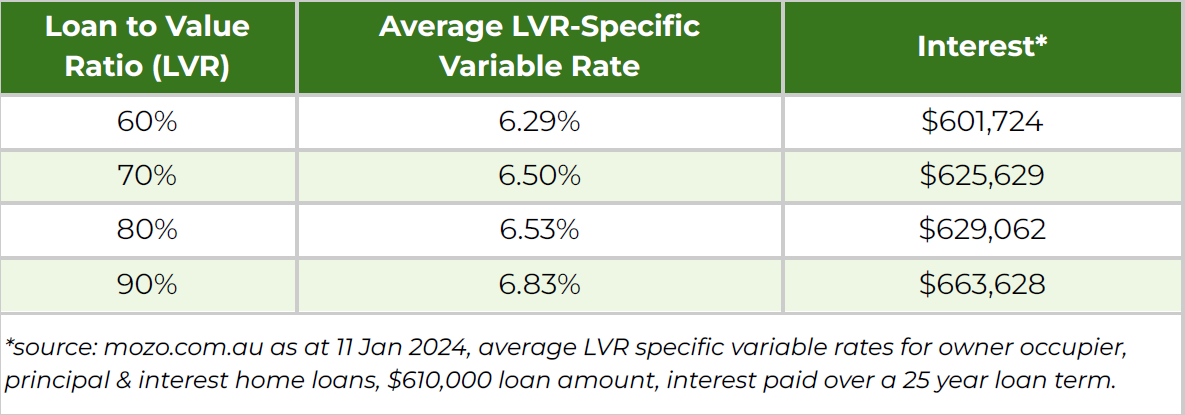

Better rates as LVR reduces

Wastell said Loan-to-Value Ratios (LVRs) can make a significant difference to the rate banks offer and mortgage holders who have been paying off their home loans for years are likely to find their LVR has reduced – however, most banks do not automatically adjust the rate as borrowers pay off their loan.

“As such, the responsibility often falls on the borrower to seek out better terms when the LVR drops to a lower tier, which many homeowners are probably unaware of,” Wastell said.

Mozo analysis shows some lenders can offer much lower interest rates for lower LVR tiers, based on LVR specific rates with the averages showing a difference of 0.54% between a 60% and 90% LVR.

That equates to a $61,904 difference in interest over a 25-year loan term.

Saoud said, in 2023, the RBA unleashed the steepest series of interest-rate increases in a decade in an effort to tame inflation – and it may not be done yet.

“We can’t speculate if and when there will be rate cuts in 2024,” Saoud said.

“That being said, nothing lasts forever – be it a low interest rate or a high interest rate environment – cycles come and go.”

Path to securing a loan daunting

Saoud the shifting economic landscape can make the path to owning a home feel uncertain and overwhelming for borrowers.

“The good news is that it isn’t stopping Australians from having goals,” Saoud said.

“Our recent Money Mindset research found 1 in 2 Australians who don’t own their own home are currently saving a deposit to purchase a property in the near future.

“What’s really surprising is that over half, or 53%, of hopeful homebuyers say they would accept a higher interest rate if it meant being approved for their home loan sooner.”

Saoud said brokers have a key role to play for borrowers in the current economic conditions which are also coupled with serviceability constraints.

“Some savvy borrowers are certainly doing their research, but ultimately, it’s the role of an experienced broker to educate and guide borrowers thoroughly through all their options – including non-bank lenders,” Saoud said.

“After all, that is the important role brokers play: providing loan options that align with their clients’ financial circumstances and long-term goals, rather than solely emphasising the cheapest rates that aren’t always available for all borrowers.”

Why is now the best time to shop around for a better loan? Share your thoughts below.