Banks intensify fight against scams with new measures and $100 million investment

The Australian Banking Association (ABA) has welcomed a new report from the National Anti-Scam Centre, revealing that collaborative efforts between the industry and the government are yielding results in safeguarding Australians from scams.

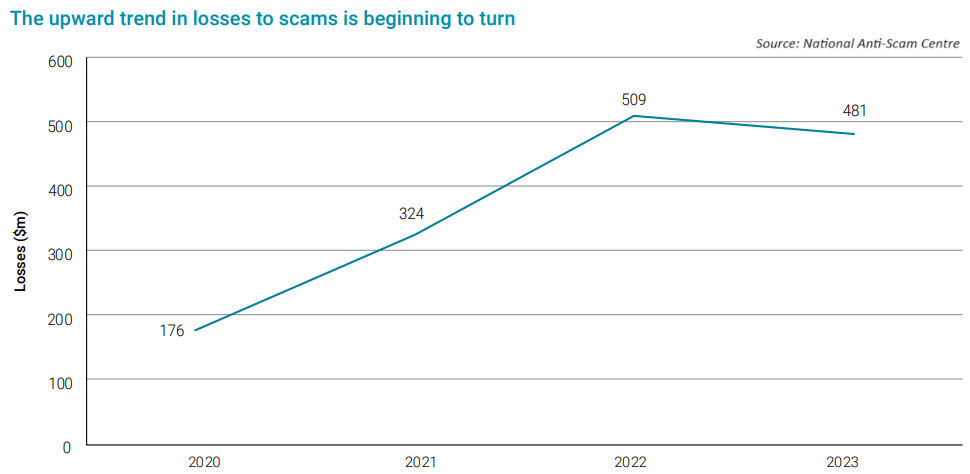

According to the latest data for the December quarter of 2023, scam losses witnessed a substantial decline of 43% compared to the corresponding quarter of the previous year.

The report highlights a notable decrease in losses across various scam categories, including investment scams (-38%), romance scams (-41%), employment-related scams (-38%), false billing (-53%), and phishing scams (-62%).

The National Anti-Scam Centre report further indicates a 74% drop in losses due to cryptocurrency scams, amounting to $12.4 million, and a 31% decrease in losses from bank transfers, totalling $40.2 million.

Anna Bligh (pictured), chief executive of the Australian Banking Association, emphasised the positive impact of concerted efforts to shield Australians from scam activities, acknowledging the progress made in the fight against scam operations.

“Unfortunately, when one scam disappears another will appear and therefore it’s critical banks, government, telcos, social media platforms as well as consumers continue to work together to stay one step ahead of scammers,” Bligh said.

The banking sector, she said, is investing heavily in advanced technologies to combat scams, including measures to block or limit transactions to high-risk crypto exchanges commonly used by scammers to transfer funds.

“Our new Scam-Safe Accord is also a game-changer and will set an even higher standard of protection by the banks to shield consumers from scammers,” Bligh said. “The centrepiece of this new accord is a $100 million investment by banks in a new confirmation-of-payee system. This will help reduce scams by ensuring people can confirm they are transferring money to the person they intend to.”

Additional measures under the Scam-Safe Accord involve the implementation of more customer warnings and payment delays, the adoption of technology and controls to prevent identity fraud, an expansion in intelligence sharing across the banking sector, and the requirement for all banks to develop and execute an anti-scams strategy to enhance their ability to detect and respond to scams.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.