National property market indicators suggest that a trough had already started forming in large city markets, economist says

After the respite of last month’s pause, the Reserve Bank of Australia has recently raised the cash rate by 25 basis points to 3.85%, continuing the cycle of rapid hikes witnessed over the past 12 months, with the possibility of further rises flagged later this year, in a bid to bring inflation closer to the target band of 2-3%.

“National property market indicators suggest that a trough had already started forming in our large city markets,” said Julie Toth (pictured above), PEXA chief economist.

“Prices and sales volumes were turning up again in April, even though the full effect of all the previous rate rises in this cycle were yet to wash through. [The] rise may cause sellers and buyers to pull back from the housing market again, as they reassess their housing options and wait for a more stable credit and pricing environment.”

Toth said the rate hikes are continuing to prompt Australians who already hold a mortgage to seek better financing solutions within the competitive mortgage market.

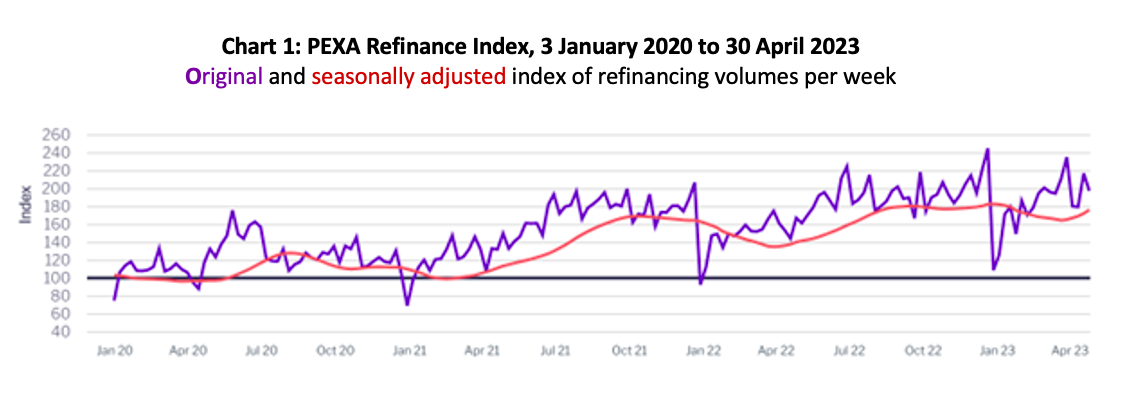

“PEXA’s Refinance Index of loan refinancing volumes confirmed strong levels of refinancing activity in 2023, following a record high month in December 2022 (followed by a seasonal lull in January),” she said.

PEXA’s Refinance Index in the week ending April 30 lifted to 175.4 points, in seasonally adjusted terms. That figure was up by 6.7% from one month earlier, up by 25.9% from the same week last year, and up by 58.9% from the same week in 2021.

PEXA’s latest research report, Emerging Mortgage Risk, found that an increasing number of Australian homeowners were battling significant rises in their home loan repayments due to the combination of recent rate hikes, steep house price increases, and the ongoing cost-of-living pressures.

“These risks are particularly pronounced for those who have recently purchased their residential property (2020 to 2023),” Toth said. “[The latest] rate rise will add directly to the mortgage repayment pressures faced by these households.

“Looking ahead, we are very close to the top of this rate rise cycle – if not already there. The RBA continues to flag the possibility of one or more further rate rises in 2023, in order to bring inflation down toward its 2-3% target band. All current mortgage holders and prospective buyers need to remain live to this possibility, and to fully factor it into their refinancing, borrowing, and purchasing decisions.”

For more information, visit the PEXA website.

Use the comment section below to tell us how you felt about this.