It may be time to put the solution in front of your clients…

This article was provided by Equitable Bank.

A reverse mortgage is a flexible financial tool that can give seniors access to more money at a lower cost than other borrowing options. It can also help a senior to stay in their home longer, which can have financial, emotional, and lifestyle benefits for them and their family.

Meet Mary

Mary lives in a house in Hamilton, ON, built in the 1970s. It’s on a large lot and is probably worth about $1 million. She’s a healthy 80-year-old widow with a modest survivor pension from her late husband, as well as government pensions and moderate savings.

She has about $50,000 of credit card debt that has accelerated since her husband’s passing and only about $10,000 of remaining room relative to her limits. They carried a small balance previously, but with a 33% reduction in his company pension and the loss of his government pension income, it’s tough for Mary to cover her fixed expenses.

Financial options

Mary’s son took her to the bank to get a line of credit. The bank was only willing to offer her a $10,000 unsecured line of credit. They said if she got a secured line of credit backed by her home equity, they could only provide a limit of $100,000 based on her income. Both of these options could help reduce her interest costs in the short term and provide some additional funds in the medium term, but may not be her best long-term solution.

Mary needs about $1,500 per month beyond her pensions, or about $18,000 per year. If she proceeds with the bank’s offer of a $10,000 unsecured line of credit and $100,000 secured line of credit, she will have $110,000 at her disposal. With it, she could pay off her credit card debt and have $60,000 of additional funds available. This might only last her for three years, before she’s back to using her credit cards. The bank also said she may need to close a couple of her credit cards to get approval for the lines of credit.

Another option for Mary is to sell her house and move into a condo. This has its benefits, as Mary is social, but the condos in her neighbourhood are primarily new and tend to be lived in by young families.

Another feature of these condos is relatively high fees for amenities that Mary will not likely use, like a gym, a pool, and underground parking. Mary doesn’t drive anymore and can walk pretty much anywhere she needs from her house.

Despite Mary’s home being older, it’s been well maintained. She’s hesitant to spend much on the house, as the next buyer will likely renovate to modernize. As a result, her home maintenance costs are modest.

If Mary bought a condo nearby, after transaction costs, she may not net much money to pay off her debt and add to her bank account. Her monthly costs could also be higher, and she would need help from family to drive to do errands.

Although Mary could sell her house and move into a retirement home, she values her independence. She’s still mourning the loss of her husband and selling the house would feel like another loss. The way Mary sees it, if she sells her house and spends the proceeds on rent, that reduces her estate value. If she stays in her home and borrows against it, that also reduces her estate value. More importantly, she and her husband worked hard to build their wealth and have helped their kids and grandkids plenty over the years, so maximizing their inheritance is not a priority. Even though home prices in her neighbourhood have appreciated, keeping her home may well end up a better investment than selling it and investing the proceeds.

The reverse mortgage solution

As an alternative, Mary could consider a reverse mortgage, which could allow her to borrow about half her home equity or around $500,000. The interest rate may not be that much different than those for the two lines of credit offered by the bank. Like a line of credit, a reverse mortgage can be flexible. Payment options include a lump sum advance all at once, regularly scheduled payments like a pension which can be deposited to her bank account, or on a per-need basis over time.

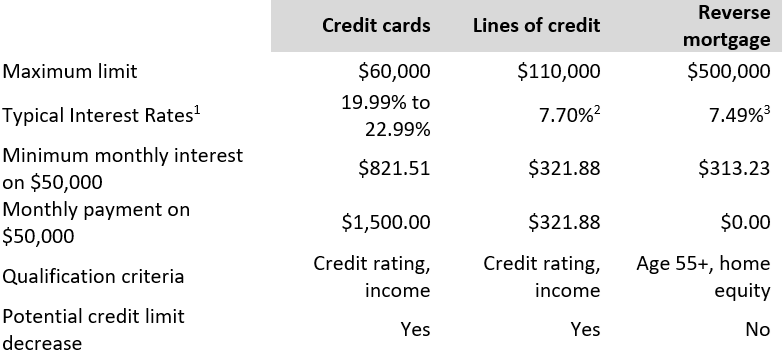

Here's the comparative math and summary for the borrowing options presented to Mary:

The line of credit interest rates are variable rates that fluctuate with the prime lending rate. A reverse mortgage has convenient variable or fixed rate options available.

A traditional mortgage loan rate tends to be lower than a secured line of credit rate by 1.0 - 1.5%. Seniors most often end up using lines of credit if they need to borrow monthly, with rates more comparable to a reverse mortgage*. Either a line of credit or a reverse mortgage could be better than a credit card for a senior who needs to borrow to supplement their spending.

A reverse mortgage may allow a senior to borrow more money than they could otherwise through traditional borrowing, and a lump sum payment from a reverse mortgage can be used to pay off other high interest rate debt or used for a one-time cost like a renovation. Some seniors also set up a recurring monthly advance into their bank account that is like a pension, but tax-free. This allows them to continue to qualify for means-tested benefits, like the Guaranteed Income Supplement, or Goods and Services Tax/Harmonized Sales Tax (GST/HST) credit, and the amount they’re eligible for based on age for Canadian pension plan (CPP) and old age security (OAS).

A reverse mortgage may not be right for everyone, but it can be a great option for many. So before downsizing, renting, or moving into a retirement home, seniors and their families should consider the flexibility of a reverse mortgage as a financial tool to help them stay in their home.

Ready to learn more about Equitable Bank’s reverse mortgage solutions and rates? Visit equitablebank.ca.

This article is provided for general information purposes only and does not constitute financial, investment, or tax advice by Equitable Bank.

1 Interest rates are as of December 4, 2023. Subject to change without notice.

2 Average HELOC rate as at December 4, 2023 on ratehub.ca. Subject to change without notice.

3 Rate based on Equitable Bank’s 5 year fixed-term Flex rate. Subject to change without notice.

7.505% APR for 5 year fixed-term Flex rate. APR means the cost of borrowing expressed as an annualized interest rate for the Interest Rate Term, based on the Initial Advance Amount, interest and any applicable fees. The APR figure is based on the following:

- A mortgage amount of $150,000 and the accumulated interest for the applicable interest rate term; plus

- a set-up fee and a closing fee (varies by province; not applicable at reset); and

- all funds drawn as an initial advance; and

- no prepayments

*At time of publication.