The impact of rate hikes is now being clearly felt, economist says

New Zealand households face mounting financial pressure, despite mortgage rate fixing delaying the impact of OCR hikes and as a rising number of borrowers are now rolling on to higher interest rates.

Satish Ranchhod (pictured above), senior economist at Westpac NZ, said many households have been insulated from the impact of OCR hikes over the past year by widespread mortgage rate fixing, but that only delayed the hit from the rising OCR to their finances.

“Around 90% of New Zealand mortgages are on fixed interest rates, usually for terms of one to two years,” Ranchhod said. “That’s meant many borrowers have remained on the very low interest rates that were on offer in the wake of the pandemic, even as new mortgage rates have climbed rapidly.

“However, while mortgage rate fixing has delayed the impact of interest rate rises, we are now in the ‘sweet spot’ for the transmission of monetary policy, where the impact of rate increases is being clearly felt.

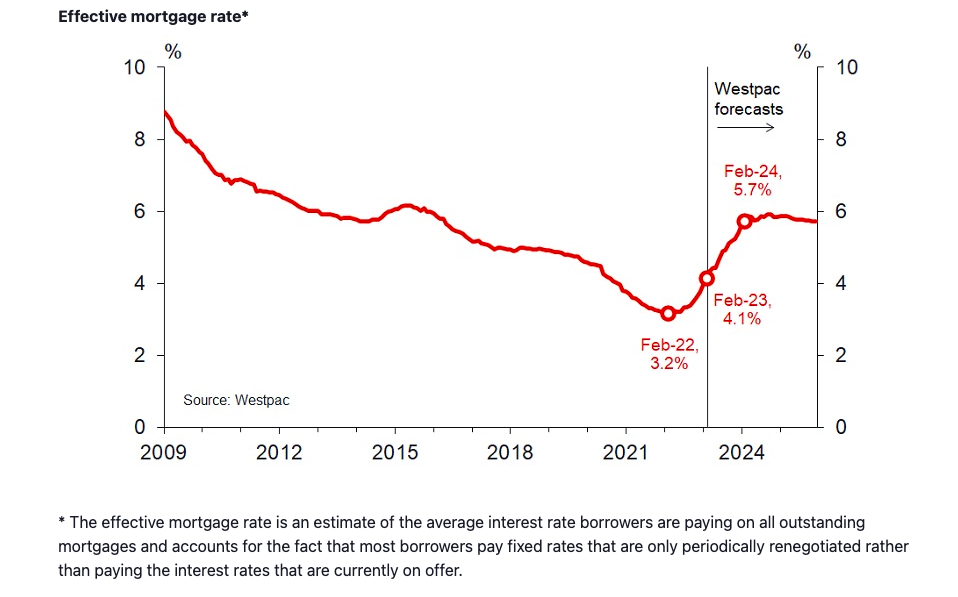

“The OCR has been rising for more than 18 months, and large numbers of borrowers have now rolled on to higher interest rates. Accounting for the extent of mortgage rate fixing, we estimate that the average ‘effective’ mortgage rate that New Zealand borrowers are paying has increased by close to 100 bps since early 2022.”

With around 50% of all fixed rate mortgages rolling onto the much higher interest rates that are currently on offer, Westpac is expecting the average mortgage rate to lift by a further 160 basis points by early 2024.

“As household finances come under increasing pressure, we expect an extended period of weak economic growth, with the economy tipping into recession through late 2023/early 2024,” Ranchhod said.

“The rise in interest rates will mean that the average household’s spending on interest costs will increase from around 5% of their disposable income in 2022 to 10% in 2024. Combined with large increases in living costs, that will suck a sizeable amount of cash out of households' wallets and will be a significant drag on household spending.

“We also expect further falls in house prices. That downturn in demand will ripple through the labour market and wage growth and will ultimately dampen domestic inflation.”

A recent Westpac paper, “From Squeeze to Crush,” looked at how the mortgage rate increases would impact different household groups, including a breakdown of mortgage costs by region.

Ranchhod said that against this changing interest rate backdrop, Westpac has been writing to around 6,000 customers who are approaching expiry on a fixed rate each month, “to discuss their options and point them to digital tools to assist with their borrowing decisions.”

The bank has also been calling customers who were facing the largest repayment increases and who might need more help.

“Westpac ask anyone who has concerns about their finances to come and talk to us early so we can assess their options,” he said.

Use the comment section below to tell us how you felt about this.