But there could be a light at the end of the tunnel for late 2023, economist says

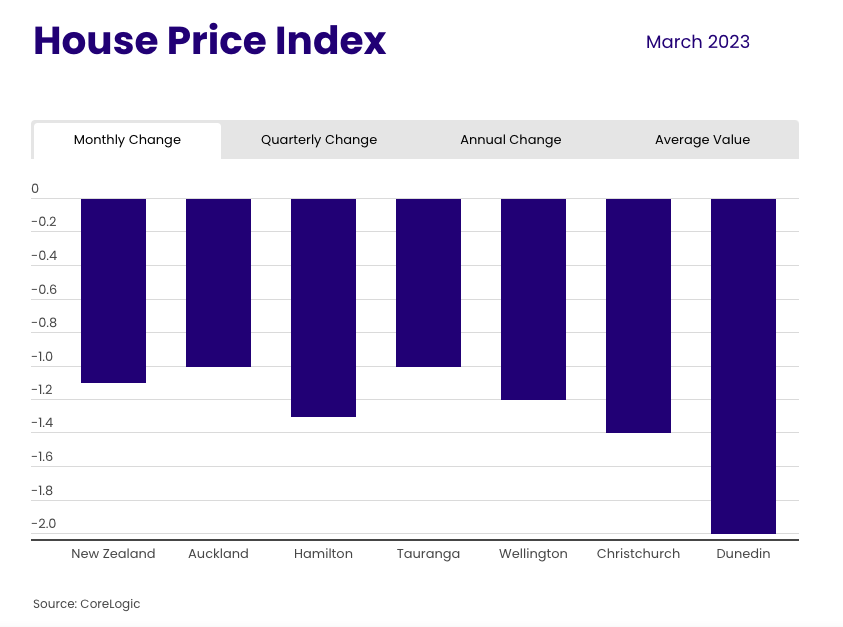

CoreLogic’s House Price index is now down 10.5% or an equivalent $109,491 over the past year, after average values dipped another 1.1% in March.

This follows a couple of flatter months in December and January, when average values slipped at least 1% for each of the past two months.

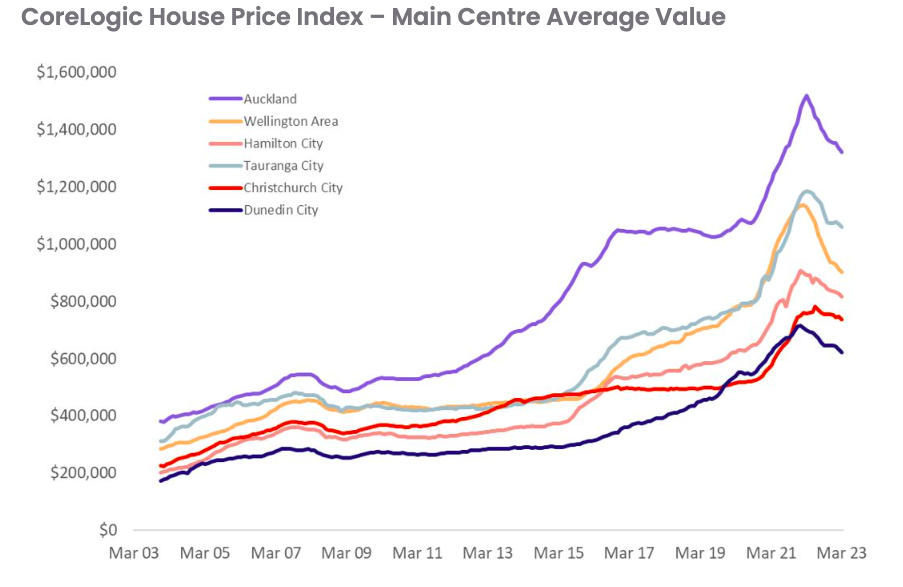

Kelvin Davidson (pictured above), CoreLogic NZ chief property economist, said the declines should be kept in context of the 43% surge between March 2020 and March 2022, with prices currently still around 30% higher than pre-COVID levels.

Prior to the latest Reserve Bank decision, Davidson said that the falls in February and March were part of the market cycle’s more recent trend and consistent with the underlying drivers.

“There are now signs of a peak for mortgage rates, while employment also remains healthy,” he said. “But interest rates for both new borrowers and existing borrowers who are repricing remain elevated, and this is requiring some careful budgeting. Mortgage availability also remains restricted and neither buyers nor sellers are in much rush, meaning market activity is low. These factors make it easy to see why property values are continuing to drop.”

The Reserve Bank yesterday delivered a shock 0.5% hike, which according to Davidson could be the last of the cycle, especially if the Q1 2021 inflation data showed a clear slowdown when released on April 20.

The nation’s main centres all saw declines in March, with Auckland, Tauranga, Wellington, Hamilton, and Christchurch down by 1-1.5%. Dunedin was the weakest, with a decline of 2% over the month.

The CoreLogic report said the key differences start to emerge between the year-on-year comparisons.

Christchurch saw average values dip by a mere -2.9% since March last year, reflecting its relatively favourable starting point for housing affordability. Wellington, in contrast, stood out with a -20% fall, reflecting its previous long boom and the stretched position for housing affordability as New Zealand entered this downturn.

In Upper Hutt, Lower Hutt, Porirua, and Wellington City, average values all fell around 20-21% over the past 12 months, with Kapiti Coast down by a lesser but still significant 15% or so.

Auckland’s property market generally continued to drop in March, although the Auckland City sub-market only slipped by 0.2%, while Franklin posted a 1.7% rise. Franklin’s average values, however, remained down by 2.6% over the past three months and by 11.1% since March last year. The various Auckland sub-markets posted annual declines in the range of 10-15%.

The results were mixed outside the main centres. In March, a number of regional property markets saw values drop by 2-3%, but Whanganui and Palmerston North avoided falls, while Queenstown rose by 1.8%. Over the past three months, areas such as Nelson and Palmerston North have been flatter as a whole, while again Queenstown has risen.

“Regional variability doesn’t come as any major surprise, given the different local factors that apply at any point in the cycle,” Davidson said.

“But it’s still quite striking to see Queenstown’s values holding up well, yet other ‘provincial’ markets declining at double-digit annual rates. In an environment where credit conditions are generally restraining activity and prices, this illustrates the power of cash/wealth in a market such as Queenstown.”

Moving forward, Davidson said the property market still faces significant challenges in the near-term, including a possible recession and the wave of mortgage repricing that still has to be worked through by borrowers and the banks, CoreLogic reported.

“The housing market ‘mood’ is pretty subdued at present, with both buyers and sellers having become accepting of tough fundamentals and lower prices,” he said. “However, the first marker for this downturn coming towards its conclusion – a mortgage rates peak – now seems to have been reached.”

“When you add relative resilience for employment, rising net migration, and perhaps some scope for investors to sneak back into the market towards election time – if they deemed a National victory and the reinstatement of interest deductibility relatively likely – there’s a case building for property sales activity to creep higher later in 2023 and for prices to stop falling.

“It’s a bit chicken-and-egg, but the current negative mindset could also shift quickly alongside those other key drivers, adding to the light at the end of the tunnel for late 2023.”

Use the comment section below to tell us how you felt about this story.