Inside Westpac NZ's half-year results

Westpac New Zealand is seeing a shift in how its customers are securing mortgages, with a growing reliance on brokers.

The bank's latest half-year results reveal a rise in broker-introduced loans from 51.9% to 53% of its total mortgage portfolio between September 2023 and March 2024.

This trend comes alongside an overall increase in Westpac's mortgage portfolio value, reaching $67.4 billion in March compared to $65.8 billion in September.

The growth is primarily driven by a rise in owner-occupied loans, which now represent 74.4% of the portfolio, up from 74.1% in the previous period. Conversely, investor property loans dipped slightly from 25.9% to 25.6%.

The results also highlighted a continued preference for fixed-rate mortgages, with 90% of loans opting for this stability in March compared to 91% in September. Variable-rate loans remain a small portion of the market at 10%.

Additionally, interest-only (I/O) loans saw a minor decrease, dropping from 16.5% to 16.0%.

These findings suggest a growing comfort level with fixed-rate mortgages among Westpac's New Zealand customers, potentially due to a desire for predictability in their repayments during an unpredictable environment.

Breaking down the numbers: Westpac NZ’s half-year results

Overall, Westpac’s New Zealand segment’s net profit after tax was up 11% ($477 million) over the half due to lower impairment charges.

Westpac NZ chief executive Catherine McGrath (pictured above centre) said the bank has invested over the period to support customers with cost-of-living challenges in a tough environment and strengthen its business for the future.

“We’re continuing to step up to support customers through a range of immediate challenges, as well as set them up for the longer term and improve their banking experience,” McGrath said.

“We’ve supported first home buyers to purchase 3,101 homes in the last six months – a 14% increase on the prior corresponding period – and we have a wide range of options in the market to help them on that journey.”

Net lending was up $AU1.5 billion – increasing by 2% against a “backdrop of subdued credit growth”, according to Michael Rowland (pictured above left), Westpac CFO.

“(Lending growth was) supported by an improvement in our product offering while business and other lending were little changed,” he said.

However, deposits contracted by $NZ1 billion with reductions in term deposits and transaction accounts.

“The decline in these accounts reflected the broader challenging economic environment.”

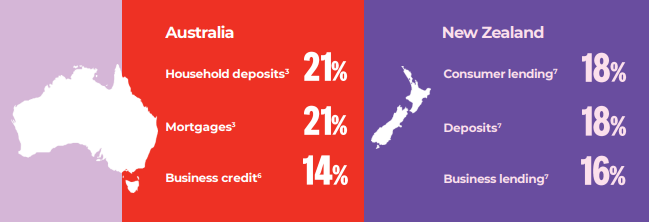

The major bank now has a total market share of 16% for business lending, and 18% in consumer lending and deposits, respectively.

Mortgage delinquencies rise

Westpac New Zealand has issued a higher proportion of loans considered riskier in recent months.

This is because they've approved more mortgages in the higher loan-to-value ratio (LVR) brackets. In March 2024, 9.2% of new loans fell into the 80%-90% LVR bracket, and 3.1% were in the even riskier above-90% LVR bracket.

These percentages are higher compared to loans originated six months earlier.

However, Westpac NZ still largely deals with the vanilla loan segment, with 92% of its mortgage portfolio having an LVR of less than 80%.

Despite this, mortgage 90+ day delinquencies have trended up, although from a very low base with 0.47% of loans falling into delinquent territory, up from 0.33% in September.

30+ day delinquencies also rose from 0.71% in September to 0.92% in March.

In comparison, Australia’s 90+ day and 30+ day delinquencies rose to 1.06% and 1.81% respectively over the same period.

McGrath said the bank has been focused on early and proactive outreach, contacting more than 51,000 home loan customers who were due to re-fix at higher interest rates in the past six months, as well as more than 1,800 customers Westpac identified as at most risk of financial stress.

“We know things are tough for businesses as well, especially in the retail and hospitality sector,” McGrath said.

“Through our internal modelling we’ve identified those most in need of help and provided a range of support, such as help with cash flow, while our free online Westpac Smarts series continues to offer practical insights and advice.”

“Overall, we have fewer customers suffering hardship than we’d expected, and most remain well-placed to manage ongoing cost pressures.”

Westpac NZ’s boosts sustainability initiatives

Westpac NZ also pointed to its many sustainability initiatives across both Australia and New Zealand in its half-year results.

McGrath said as well as helping with short-term challenges, the bank was focused on helping customers tackle longer-term challenges such as climate change in a way that enhanced their business or home environment.

In particular, the bank said it supported 426 unique New Zealand customers with labelled sustainable loans worth $5.2 billion as of March 2024, with $2.4 billion in the agricultural sector alone.

The results came one day after Westpac NZ has unveiled a new sustainable equipment finance loan.

The initiative offers a competitive five-year financing option for the purchase of sustainable assets such as electric or hydrogen-fuelled vehicles, and other machinery and tools that contribute to lowering a business's carbon footprint.

This comes after the bank released its Westpac New Zealand Climate Report with banks on notice about the repercussions of climate risks on banking.

Westpac NZ’s economic and housing outlook

In Westpac’s outlook, Westpac CEO Peter King (pictured above right) said the bank is “well positioned to navigate the prevailing environment, and support customers that are facing challenges or looking to grow”.

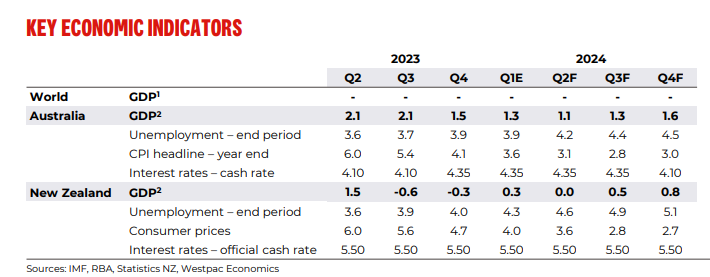

Westpac forecasts New Zealand’s GDP to slowly recover from its recent recession as consumer prices continue to decline. However, unemployment is expected to rise throughout the calendar year.

Therefore, the major bank expects no changes to the official cash rate (left at 5.50%) for the rest of the year.

Westpac also expects national dwelling prices to increase by 6% in the 2024 financial year and a further 7% by FY2025.

Nationwide, New Zealand has averaged 8% annual growth over the past decade.

McGrath said a sluggish economy, weakness among key trading partners such as China and a tense geopolitical environment are all contributing to uncertainty across the economy.

“The dominant narrative right now is that economic weakness and tight financial conditions are weighing heavily on households and businesses,” McGrath said.

“The next few months will be critical for getting businesses and communities on the same page to start unlocking our potential.”