Customer-owned banks work closely with brokers on lending solutions

It’s been another challenging year for the mutual banking sector, but once again the banks’ ability to adapt to changing customer needs and build on strong partnerships with brokers has paid off.

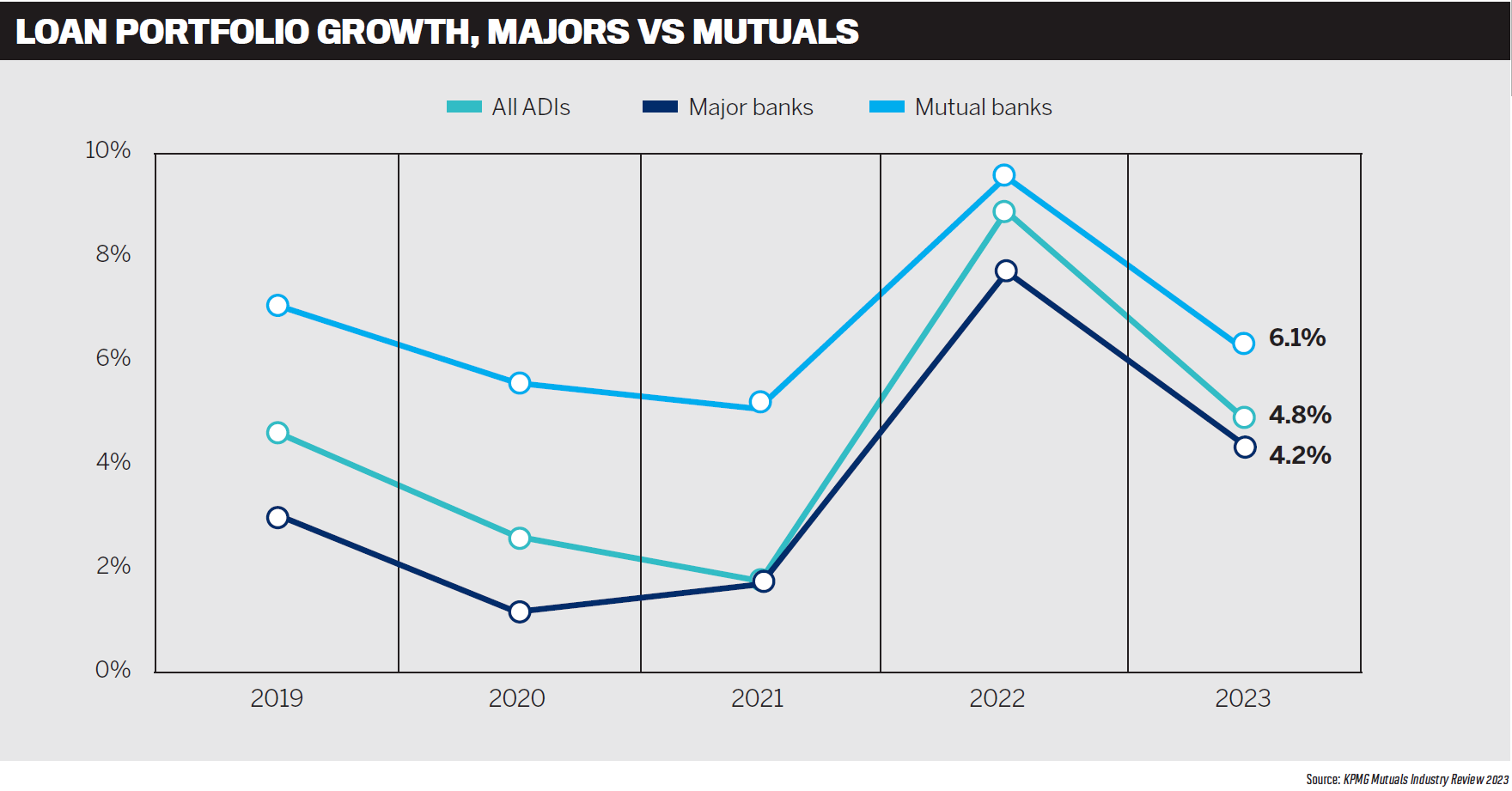

Despite aggressive competition from the major banks, which pursued new customers through cashbacks, customer-owned banks outperformed their bigger rivals.

The KPMG Mutuals Industry Review 2023 report revealed loan portfolio growth of 6.1% for the sector, compared to 4.8% for the major banks and 4.2% for all banks.

Customer-owned banks worked hard, in conjunction with their broker partners, to assist customers struggling with higher interest rates and inflation, offering the best rates possible to those rolling off fixed rates onto variable loans.

Staying close to their customers and broker partners and being responsive and upfront about their value proposition assisted with customer retention and maintaining market share. Other factors, such as green lending, ethical investment and ESG, also attracted new business.

While processing and turnaround times continue to be a challenge, customer-owned banks are determined to lift their game in this area, investing in new technology.

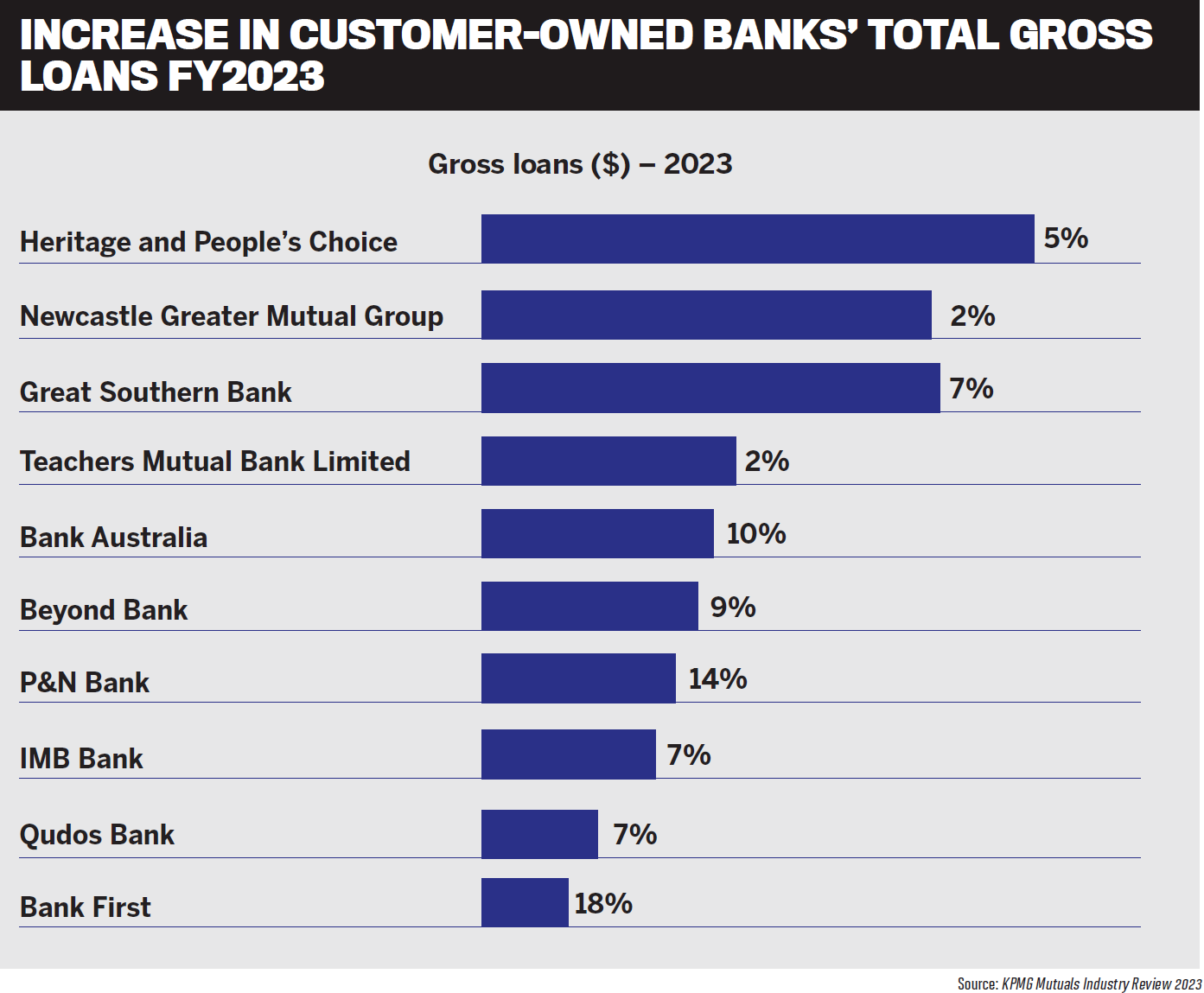

In 2023, Greater Bank and Newcastle Permanent merged to create Newcastle Greater Mutual Group, while Heritage Bank and the People’s Choice Credit Union also merged, with the brands to be unified under the name People First Bank.

To discuss these and other issues, third party leaders from top customer-owned banks Bank Australia, BankVic, Beyond Bank, Gateway Bank, Heritage Bank, Newcastle Permanent, P&N Bank and BCU Bank and Teachers Mutual Bank Limited attended MPA’s annual industry roundtable, held at Woodcut Restaurant in Sydney. Also taking part in the discussion were mortgage brokers Jennifer Lemme from Liberty Network Services and Mandy Hill of Mortgage Managed.

Q: In a year of rising interest rates, higher inflation and reduced borrowing capacity, how have customer-owned banks and their broker partners risen to these and other challenges?

Zeb Drummond (pictured below), chief operating officer at Gateway Bank, said brokers and lenders in partnership had done a really good job of bringing customers through this challenging experience, “something that they likely haven’t faced before”.

“You list off all the pressures, and brokers at the coalface are trying to manage expectations of customers and trying to, in some instances, get them into market in an environment where historically it’s been running away from people,” Drummond said.

In a higher interest rate environment with loan buffers, “it runs away even faster”.

Drummond said for customers this meant loan approvals ‘in principle’ that were expiring; reassessments; and potentially reduced borrowing capacity.

“That person’s dream right in front of your eyes slips away. For us, it’s been about acknowledging that and trying to support brokers managing those customers’ expectations and trying to meet them.”

This involved listening to what customers and brokers were saying and honouring, wherever possible, “what we said we were good for”, Drummond said.

“Let’s find a way to continue to honour that approval in principle so that we’re not snatching that dream away from people.”

Drummond said this approach was well received by brokers.

“It’s what I would like to have happen if I was a consumer. Just appreciate that it’s me trying to buy a house for my family, not just a number on a piece of paper. See that I’m good for it; help me do it.”

BankVic head of distribution channels Jay Farrell (pictured below) said the bank was new to the broker channel, “so navigating the differences between working directly with members and via brokers has been a great learning experience”.

Echoing Drummond’s comments, Farrell said BankVic was focusing on building its relationships with brokers in order for them to be able to educate their borrowers about a BankVic home loan.

“The key for us has been working with our brokers to make sure they are comfortable with our product mix, how we work and the assessment criteria we require. We want to make sure that they are comfortable with our end-to-end process and who BankVic is – so it’s not just about the rate.”

Farrell said BankVic had just come out of testing with one aggregator and now had a national broker offering.

“It’s been a slow burn for us because we want to make sure we get it right”

Mark Middleton (pictured below), head of third party distribution at Teachers Mutual Bank Limited, said it had been a “really interesting year of two halves for both banks and brokers”.

He said at the beginning of 2023 a lot of loans went to banks offering cashbacks, particularly the majors.

He said at the beginning of 2023 a lot of loans went to banks offering cashbacks, particularly the majors.

“That would be hard for those brokers, as well as the banks, when you’ve got someone sitting in front of you – where do you direct the right solution for those customers?

“We’ve found that as cashbacks came off during the year, [loan] flows went up substantially during that period, and then it’s trying to manage those flows from an SLA perspective.”

Middleton said it had been difficult for TMBL to manage the expectations of brokers as the focus went more towards refinances, and turnaround times rose.

“We had to be honest and tell brokers, if you’ve got a purchase it’s going to make it really hard – we don’t have that queueing system of purchase versus refinances, and our flows went up 300%,” Middleton said.

TMBL also had to cope with high customer demand for the Home Guarantee Scheme.

“We’ve changed our focus away from fixed rate products to variable rate products. This has rebalanced our portfolio for the future and produced better margins.”

Middleton said all customer-owned banks appreciated working with brokers – a core part of their businesses.

Newcastle Permanent head of digital product development Simon Burt (pictured below) agreed with Middleton about 2023 being a year of contrasts and banks needing to understand how they should position themselves in the market.

“Last year in this forum we were talking about the fixed rate cliff,” Burt said. “Part of that was the shift away from the majority of new business as fixed into a much more variable mix.

“We all have this challenge of trying to find that balance between the right level of pricing to drive our first party business, and broker.”

Burt said the broker sector had performed strongly for Newcastle Permanent over the year. “We’ve also had a lot of success in that retention space. We wrote a lot of those customers on fixed rate loans to brokers, and new customers to the bank.”

Burt said the bank had worked hard to retain customers when their fixed rates rolled off onto variable rates.

“We’ve done really well in that space, looking after our customers, ensuring they have the best options presented to them at roll time for their situation.”

Burt said that in terms of broker partnerships, one of the challenges for customers had been borrowing capacity as rates rose and capacity reduced.

“We continue to get feedback from our broker partners. Staying close to them through our BDMs is really critical, and making adjustments to policies, process and products to continually evolve.”

Darren McLeod (pictured below), head of third party at Beyond Bank, said the bank had enjoyed a record year of third party lending, with 50% of total volume.

“We only started dealing with brokers seven years ago, and that volume is not bad in that short space of time,” McLeod said. Brokers enjoyed more than 70% share of the residential home loan market.

“We had a record year, so our focus has been on making sure we’ve got competitive prices, products and features,” McLeod said. “The results speak for themselves. As a smaller lender, you’ve just got to make sure you take your opportunities when they come.

“We had some good pricing and products for the last 12 months. Our first half of the year was a lot of first home buyers through the NHFIC scheme.”

McLeod said that in the second half, when Beyond Bank wrote most of its volume, cashbacks dissipated, “so our refinances really increased”.

“We’re also quite aggressive on investment, because our book was a bit skewed towards owner-occupied, so in the last six months we’ve written lot of investment [loans] as well.”

Beyond Bank’s biggest challenge had been keeping up with service and turnaround times, McLeod said.

“2024 is the year of improvement for us. We’re investing heavily in technology, structure, processing, etc, so we can still have these competitive products and pricing and turn them around as brokers expect.”

Heritage Bank head of broker and business banking Stewart Saunders (pictured below) said that from a customer perspective, “it’s been an incredibly challenging year with increasing costs across the board”.

“Homeownership is the largest component in most households’ cost base, and that’s increased significantly over the year,” he said. “Low fixed rates coming off has been really challenging for many households with significant increases in repayments.”

Saunders said customer-owned banks had remained competitive on pricing and by supporting customers coming off fixed rates.

“Brokers are so instrumental to how mutual banks really do work to support those customers. You see it coming to the fore now. It’s coming through in the growth numbers for all of the mutual banks.”

Saunders said banks were working with brokers to help first home buyers, refinancers and investors, and existing customers facing servicing issues.

“Working with brokers and customers to get better rates and options has really helped all of us and means that fewer people are facing hardships. This is where mutual banks and brokers are so fundamentally aligned, because we’ve all got the customer’s best interests at the heart of what we do.

“As a mutual bank, our members are our owners. That’s why we always have our customer’s best interests as our top priority, just as brokers do under best interests duty.”

Saunders said customer-owned banks didn’t have the challenge of trying to maximise profits for investors. “This is not about the best price for one customer; it’s about the best price for all of our members.”

Broker support was shifting to the mutuals, and brokers were offering them as a competitive option for their borrowers.

“We’ve now passed five million mutual bank customers across the sector,” said Saunders. “One in five households are now banking with a mutual, which is great to see.”

Saunders said customer-owned banks had more than 720 branches across the country, which was 18% of the total branch footprint. Of all the banks represented at the roundtable, 52% of staff from mutual banks worked in non-metro areas.

“It’s the overall service offering that mutuals provide which has really been recognised by customers,” he said.

Bank Australia had also grown considerably over the last year, said national manager broker Matthew Wood (pictured below).

“Our annualised growth rate is currently at about 22%; and 70%, from a settlement perspective has been attributed to brokers,” said Wood.

“Brokers have really stood up in the last year. Their communication and their strategies – talking well in advance to those clients coming off fixed rates, to me was quite impressive.”

Wood said Bank Australia had worked extensively with brokers throughout the year, and “we’re getting the benefit of it”.

More time and resources had gone into ensuring that customers’ financial wellbeing “was being looked after, between us and the broker”.

“I think in the 2023 financial year, we only had 0.3% in financial hardship within our portfolio. The brokers are looking after their clients, and we’re emulating that as well.”

Kaine Adamson (pictured below), general manager broker at P&N Bank and BCU Bank, said that in a challenging economic environment with household budgets already under increased pressure, consumers wanted to turn to banks they could trust for support.

“I believe that as part of the customer-owned sector, putting people before profits is a fundamental value shared by everyone at this table,” Adamson said. “As a customer-owned bank we’re not focused on delivering dividends for shareholders, instead passing our profits back to our customers through competitive interest rates for the life of the loan.”

Adamson said that with a number of customers coming off fixed rate mortgages, it was natural to see increased concern about repayment shock.

“Our brokers were telling us they were spending a lot of time repricing their existing customers, diverting their focus from generating new business. We asked ourselves – what’s a way that we can solve that?”

So P&N Bank launched a new revert product for all new and existing customers to roll onto once their fixed rate matured, with a rate that matched its competitively priced advertised rates.

Adamson said that across the industry, fixed-rate customers typically transitioned to a standard variable rate product, which often carried an interest rate between 1% and 3% higher than advertised rates for new borrowers.

“Not only was this a way to reward the loyalty of our existing customers, but it has also alleviated some of the strain borrowers have been experiencing and has saved our brokers countless hours of having to negotiate better rates on behalf of their clients. It’s good for our customers, it’s supported retention, and we believe it’s a win-win for everyone involved.”

Servicing was also getting tighter, and brokers were struggling to find out where a deal would fit, Adamson said. In response, P&N Bank partnered with Quickli, getting the bank’s servicing calculator onto the platform, saving brokers more than 30 minutes per deal.

Broker Mandy Hill (pictured below) said customer-owned banks really looked after customers, and she used them on a regular basis.

“You’ve really come to the market with your retention rates, offering great interest rates right off the bat,” she said. “With other lenders I have to really fight for that, which takes up a lot of our time. It just creates a better customer experience because they feel like you’re showing loyalty to them.”

Hill also praised the retention rates, some of which were better than what was advertised. “I’ve definitely felt very supported by the customer-owned banks in that space over the last 12 months,” she said.

Mortgage adviser Jennifer Lemme (pictured below) said she was a big believer in supporting local small businesses. She was referring more clients to customer-owned banks, and they were easier to get in touch with.

“You can reach out to assessors; you can have a discussion. It’s just not a decline; you can talk things through,” said Lemme. “Especially with servicing calculators and borrowing capacity – anything they could possibly do just to get a deal over the line.

“They’re just nice. They get back to you straight away. You don’t tend to have that touchy-feely experience with the majors.”

Lemme said customer-owned banks were more supportive of brokers than other lenders, and the customer service was more personalised.

“I think the after-loan customer care is great. If there’s an issue, they can ring up. A lot of clients with the majors, they get someone overseas or they never get back to them.”

Hill said customer-owned banks were a long-term solution for clients because of their retention policies.

“When I’m offering that long-term solution, it’s a win-win situation for everyone. It’s a win for Heritage Bank, for example, because you retain the business. It’s a win for Mortgage Managed because I’ll retain the business. It’s a win for my client because they’re still getting a really attractive offer.”

Middleton said the difference for brokers compared to dealing with a big bank was that “we know who you are”.

“You get to know from looking at the flows coming through which brokers are supporting you.”

Due to the mortgage cliff, all customer-owned banks had made a concerted effort on retention, Middleton said.

“How do we protect our portfolio? The difference probably to an ANZ or a CommBank is they’ll go right through the process, [say] here’s your best price, and at the last minute they change their mind and give you a better price.”

Unlike the big banks, Middleton said TMBL was upfront about the retention rates it could offer brokers, which were below the published rate. “We really do want to look after the customers you’ve got, [rather] than trying to bring on a new one.”

Hill said this was a massive point of difference for brokers and a time-saver.

Burt said all the mutuals had a similar approach, which had built a lot of trust with brokers.

McLeod said Beyond Bank had always been transparent and upfront about its rate sheet, with no “trickery” involved.

Hill said she just wanted banks to tell her their best price.

Giving an example of a rate pricing from a major bank, she said she went through the pricing tool and “then they gave me the best choice, I escalated it, and they still didn’t come back with a very competitive offer. I went to my relationship manager, and I said, ‘Surely you can do better here; either that or I’ve got to take them elsewhere, because it’s not the right thing by the client’. ”

Hill was told to ring the retention team “as if they [the customer] is leaving”.

“So, I’ve done a pricing request, I’ve done an escalation, I’ve contacted my relationship manager, and then I have phoned the 1300 number to speak to the retention team as if they’re leaving – and then they dropped the rate.”

Hill labelled this process as “absolutely ridiculous”. With mutual banks, it was one email or phone call, “and then I get a result and I can move on”.

Saunders said this trust between brokers and banks was fundamental. A Roy Morgan report focusing on trust and distrust revealed that the customer-owned banks collectively scored better than any bank in Australia in terms of positive trust.

Q: In a highly competitive home loan market, how have you maintained or grown market share? What role have brokers played in this growth?

Wood said Bank Australia had experienced excellent growth in the last 12 months, with 70% of its settled loans coming via brokers in the current financial year to date.

“What we’re hearing from brokers and customers is that people are wanting to deal with an ethical bank, and we expect that our reputation as a for-purpose bank, in addition to our competitive products and high-quality services, will help us to continue growing strongly,” he said.

“That’s a big driver for us – 50% of our new clients are coming through our socially aware target market; that’s who we’re targeting.”

Surveys of new customers had shown that being socially aware was what had attracted them to Bank Australia, Wood said.

Brokers were also becoming more aware of what Bank Australia could offer when it came to clients wanting a green loan or who wanted to know where the bank placed its investments.

“We call it clean money because of what we invest in. We won’t invest in fossil fuels or gambling or the tobacco industry. We are investing in renewable energy projects, not-for-profit organisations, housing for people with a disability, and people are wanting to be a part of that.”

Wood said clean money “for the force of good” was drawing clients in.

“The next 12 months will be interesting. BID has a bit to play out. At the moment, best interests duty is still very closely aligned to rate and service.”

But Wood said BID could be expanded to include environmental and ethical factors.

“Is putting a client to a major really what they want? Is that in their best interest, or is it being socially aware and wanting to support a company that won’t invest in fossil fuels, for example? Should that be part of BID?

“If we go down that path and see that grow further, I think that’ll tie in nicely with what this group of mutuals have to offer.”

Wood said being socially aware was a good differentiator for the bank in such a commoditised market. “Differentiating on price will result in margin compression.”

Bank Australia had historically always been funded from “within”, through deposits, but due to its large growth it had to go to the markets for funding, further eroding margins, Wood said.

“Writing volume for the sake of volume is probably not the answer for us. We’re looking at writing smarter volume, leveraging the green element or the ethical play to attract new clients at improved profitability.”

Drummond said the environmental focus was very interesting.

“Broader than our industry, corporations and organisations have been held to account for their green impact, or their environmental impact through things like ESG,” he said. “When it comes to our industry, we’re going to start to be monitored and managed on what the impacts are of our mortgages, what our security is and how that performs.”

Drummond agreed with Wood’s point about BID.

“The narrative or the conversation does need to shift, because it’s going to have to shift for us as well. I’d love to think that consumers were aware enough for it to be a buying factor in their decision-making, but I think it also has to be driven by us a little bit to increase the awareness.”

Drummond said Gateway Bank was “smoothly aligned” in this area and relied heavily on brokers to impart its message to the end consumer “before we even have the opportunity to talk to them”.

“As an industry we’re getting close to 70% from a broker distribution perspective; Gateway’s business is close to 80%. I don’t have a business without broker.”

Drummond said customer-owned banks needed to focus on ensuring brokers understood the environmental responsibilities of both banks and consumers.

“Otherwise, we’re all going to be sitting in limbo waiting for something to happen, and we’ll be told what needs to happen as opposed to us driving the change. You know the old saying, ‘do or be done’? We certainly don’t want ‘to be done to’. So we need to make some changes.”

Adamson described the home loan market as one of the most competitive channels in banking, with competition among brokers and lenders at an all-time high.

“For any organisation to stay relevant and grow, you have to listen to your customers,” he said.

Adamson said broker feedback was important to P&N Bank, with improvements to processes “made as a direct result of what brokers have told us”.

“We take our brokers’ feedback seriously and believe that investing in their suggestions is key to providing them with a faster and more consistent experience that retains the all-important personal connection,” Adamson said.

“Pleasingly, these investments have resulted in a notable increase in market share, with our retail loan book growing by 13%, while the value of broker loans grew by 24%.”

Middleton said more clients and brokers were starting to look at TMBL’s ethical stance and B-Corp Certification status.

“We’re having brokers contact us because of our credentials,” he said. “Bank Australia certainly leads a lot of that in the green space; Teachers Mutual Bank Limited leads in the ethical space. We’ve won a number of ethical awards over the last 10 years.”

Consumers were becoming more socially aware and wanted to align with ethical banks, Middleton said. “This is a big thing that we’re starting to see from our brokers too.”

Wood said many brokers aligned themselves with those values, so “it’s a pretty easy sell”.

Middleton said that over the last six months as servicing got tighter, more business had come through from service workers. This required an understanding of their income streams and allowances, and the development of policies to suit that sector.

“The investment market’s becoming really tight. A lot of people will be out there doing 80% lends for rental income. Do you really need to be at 80% when vacancy rates are at 90%, 95%? Why are you needing to be at that level of 80%?”

Middleton said TMBL, like other banks, was looking at this and realising it needed to be nimbler on credit policy.

“With us having a new CEO at TMBL, he’s starting to challenge this: why is the policy that way? I’m confident you will see change.”

Saunders said there was another element that hadn’t been mentioned.

“If you look at mutual banks, historically we’ve been much smaller organisations [and] regionally based, [with] a lot of direct lending, not particularly in the broker market,” he said.

Saunders said Heritage Bank had been in the market for 25 years and was one of the first to operate in the broker sector. “We’ve experienced that growth. But banking is really a scale business. We’re seeing mutual bank mergers now providing organisations that are larger and can deal with more brokers and support their needs.”

Mergers had built a foundation for more mutual banks in the broker market, and lending growth rates were soaring.

“We’ve seen some large mergers over the last 12 months, which are creating now national organisations, which can support brokers in the market.”

Saunders said strong growth in the mutual bank sector would continue, driven by ongoing broker growth, customer choice and the service brokers provided.

Q: Broker question from Mandy Hill: Customer banks are leaders in strong customer service and retention pricing. But processing could improve – it’s unnecessarily painful for brokers and clients compared to others, and service times can be an issue. Is there anything in the pipeline to improve in these areas?

“Absolutely,” McLeod said. “That’s probably one of our main issues – we’ve got great products, great people, but it’s processing where we need to work on.”

He said this would be a big focus for Beyond Bank in 2024. “We’ve got a whole new loan origination platform, with the ultimate aim of producing quick turnaround times. In conjunction with that, we want to be auto-approving a lot more loans. We are working on a project now that will see a significant increase in the amount of loans auto-approved in 2024.”

He said this would be a big focus for Beyond Bank in 2024. “We’ve got a whole new loan origination platform, with the ultimate aim of producing quick turnaround times. In conjunction with that, we want to be auto-approving a lot more loans. We are working on a project now that will see a significant increase in the amount of loans auto-approved in 2024.”

McLeod said the bank also wanted to increase its number of electronic valuations to assist in quicker turnaround times. “We have made some policy changes which will significantly improve the amount of desktop valuations we do.”

The focus was on better technology, especially for the easier loans, which should be processed quickly. “It’s the more difficult ones that need more time,” McLeod said.

“That’s our focus. Everything you’re saying is correct. We realise that, and we’re working on it. We’ve got eSign for all documents now. We have also partnered with FMS to digitise and simplify our mortgage fulfilment process with a view to get to straight-through processing.”

Farrell said BankVic had also made digital transformation a key focus of its broker strategy. He said identification had previously been a pain point for members, requiring them to meet ID requirements up to three times in the loan process.

“We’ve now implemented NextGen ID, which means only one ID verification. It’s been a game-changer for us,” Farrell said.

“One of our pain points was living expenses. We continue to improve the process to fit in with our risk profile while improving our time to ‘yes’. This means a better user experience for our members.

“Because of our size, we’re able to be agile and adjust to the market more quickly than the bigger banks.”

Burt said one of the things Newcastle Permanent wanted to explore in the broker space was digital data capture to pre-populate applications.

“What we’ve learned is using digital data capture is a highly efficient way to capture the data for an application if you’re pulling in someone’s income, expenses and liabilities straight off their bank statements rather than both brokers and our teams manually reviewing statements.

“There is a downside in that you get all of their one-off expenses as well, but we’ve learned from our experiences how to navigate that without creating unnecessary rework.”

Q: Broker question from Jennifer Lemme: One of the key challenges is the issue of customers moving between lenders during refinancing, particularly in the first two years and [with] associated clawback. To benefit all parties, what products, incentives or strategies can lenders provide to assist brokers in retaining these customers?

Lemme said she was finding it difficult to get better rates for those coming off fixed loans.

“For some reason, a lot of lenders don’t really look after their existing customers. Our customers are coming to us and asking, ‘Can you get a better rate?’ If they are a new customer to a lender, they’ll get a better rate than an existing customer. They’re not being rewarded for being that existing customer.”

Farrell said BankVic had dropped its SVR and BVR, with members reverting straight back to its best variable rate in the market.

“Also, for our other members coming off the fixed rate cliff, we actually extended the $10,000 maximum fix for six months and let them pay down as much as they could during that period of being on that lower rate.

“We want to make sure our members coming off fixed rates are in the best possible position,” Farrell said.

Lemme said there were a lot of people refinancing to reduce their balance and payments. “It’s a big thing – they could be saving a couple of hundred dollars a month, which in this economy with inflation that’s just hit the roof is a big deal for families.”

Drummond said everyone around the table had taken action on revert rates, and this was where “we can add value for our membership”.

“I think an increased revert rate is a trap for a lot of people. It doesn’t align with the customer-owned banking mantra at all.”

He said the banks needed to be better partners to brokers by helping them manage their loan portfolios.

“For brokers facing clawback, our team calls the broker and says, ‘Do you realise that your customer’s refinancing? If you’re doing it, that’s great, we’re happy for you to do it, you’re doing the right thing.

“If it’s going to another broker or it’s going to another lender direct, we need you to know. Maybe you want to call your customer and reconnect, because they have the hearts and minds of our customers as well as we do. Brokers can broach that conversation much easier than we can.”

Lemme said she was upfront with customers. “I always say, if you’re thinking about moving, please give me the opportunity. I tell them, “If you do this [refinance] within two years, I have to pay commission back. And they go, ‘What?’ They don’t know. So it’s educating clients around the clawback.”

Q: What is your strategy when it comes to adopting AI and automation in your credit decisioning, loan systems and processes? How can this improve efficiency, speed and broker partnerships?

Burt said technology was something “we all need to be lookinig at”.

“How can we can leverage AI to streamline processing to get simple loans through faster?” he said.

Lemme asked if the customer-owned banks thought AI would cause more issues.

Saunders said it was a hugely exciting time to be a broker. “You’ll look back on these days as the dark ages,” he said. “We’re on the precipice, and the foundations are being put in place at the moment.”

He said all the banks had a huge amount of work to do. “As mutuals, with smaller budgets, the challenge is how do we partner with technology providers to be able to help us deliver?”

The Consumer Data Right and open banking had provided a platform for significant changes in the sector, he said.

“The technology that we can use to efficiently provide a significantly different experience for brokers and their customers is very close,” Saunders said.

Heritage Bank was working on how to include open banking and change policies accordingly, so “we don’t have to ask for three months’ bank statements and validations”.

“The challenge is how do we get there quickly when we don’t have the investment envelopes that the large banks do.”

Saunders said Heritage’s technology partners were keen to provide support.

“It’s a big challenge for us, but I think a really exciting one to face into. There’s lots of work being done.”

Farrell said all the customer-owned banks were investing in technology. “A lot of the transformation takes place behind the scenes, so members won’t necessarily see these changes immediately, but it all goes towards improving the overall BankVic member experience across channels.”

McLeod said brokers would “ultimately make the decision because, if we don’t fix it, you’ll soon get sick of it and go elsewhere”.

“You’re the litmus test because you’ll stop using us if it becomes such an issue. It’s up to us to get with the program.”

Burt said that when it came to artificial intelligence, it was important to focus on using the data first because “AI is really good when it comes to data”.

“AI continually learns how to do that better and better. But I think we’ve got to get over that data hurdle first.”

Drummond said, “AI is not there yet. It’s so infantile, and everyone’s understanding of what is AI and its applications… we can go around the table, and everyone will say something different.”

He said the opportunity lay in working with tech partners to develop what AI could actually do.

“This is where mutual banking and smaller organisations really add value in their spaces,” Drummond said. “We are nimble; we’re not as big. There’s not this giant ship of a major bank that has to turn to adopt to technology changes.

“We can be the testing ground for a lot of these things. We can flesh out, does it work? Does it add value? Is it right? Is it wrong? We know we’re close to our brokers, we’re close to our customers. Is it working? Yes or no.”

McLeod said Beyond Bank worked with tech firm Elula on customer retention using AI.

“Elula’s retention product Sticky enables us to identify customers who may be looking to leave or may be unhappy with the service they receive and proactively engage these customers.

“This delivers better outcomes for customers and maintains a strong ongoing relationship and reinforces the broker’s initial recommendation to put us as an option for their home loan.”

Middleton said TMBL hadn’t gone down the AI path too far but was using bots in some processes to try to speed them up.

“It’s early days. We’ve even tried to use the bots for our accreditation process and make it instantaneous, but it fails at certain points because not everything is the same.”

Bots were used once the loan application was completed through ApplyOnline, Middleton said. The data was placed into the loan origination system and bots audited the documents.

“So we’re starting to try and look at making our processes a bit smarter. I think everyone over the next 12 months to two years will be looking at process.

“Our new CEO is customer focused and is working hard to identify how we can improve our processes to make it really quick.”

Q: What are you expecting to happen with interest rates and the home loan and property markets in 2024? How are you preparing for this?

Adamson said that when it came to the stress customers faced with cost of living pressures and rising interest rates, P&N Bank wanted to be consistent in what it offered them “to ensure we’re always putting our best foot forward”.

“Irrespective of what happens with the RBA, we aim to align our lending practices with current economic conditions to ensure we operate a sustainable bank that caters to the needs of our customers both today and in the future.

“We don’t want customers for two years; we want them to stay with us for 30 years because we look after them.”

Wood said that interest rates had definitely stabilised, and inflation was starting to pare back.

“The RBA have done a lot of heavy lifting, so they won’t be in a hurry to reduce the cash rate,” he said. “I think the second half of this calendar year that will start to happen.”

Wood said he believed that while interest rate stability would give some vendors the confidence to list their properties, real estate stocks would remain low, and demand would outweigh supply. Housing affordability would also continue to be a problem until the cash rate started reducing.

“It will be an interesting period,” Wood said. “Growth will likely be moderate in terms of house prices overall; however, supply and demand in particular areas could see stronger growth.”

Wood said Bank Australia was preparing to launch a new origination platform in July. “That’ll see a large improvement in what the brokers experience when dealing with Bank Australia.”

Most banks this year would also start focusing on margin repair, he said.

“There will definitely be a switch. A lot of the special offers, they’re gone. I don’t think you’ll see them come back. I don’t think you’ll see cashbacks re-established. It’ll be about the margin repair in 2024,” Wood said.

Middleton agreed with Wood’s comments about interest rates.

“I think cuts will probably occur in the back end of the second half, probably around August, September, depending on the inflationary rate controls we have. What will be interesting is, will borrowers still be stressed at that point? Will they start making decisions? If they bought at the property peak, do some of those investment properties then start getting offloaded to ease their situation?”

Middleton said this might create an opportunity for buyers to enter the market and ease the rental crisis.

“I’m not saying it will definitely happen, but it might.”

Saunders said the economic environment would continue to be a challenge for customers.

“While interest rates will come off, property prices will still continue to increase,” he said. “They’ve continued to increase in an increasing rate environment. They’re not coming off any time soon.

“What I think we’ll see is that good brokers that look after their customers, that are doing annual reviews, that are supporting them through challenging times, will do really well in the year ahead.”

Saunders said the brokers who were focused on refinancing and not on supporting and servicing their existing book would struggle.

“For those that have a really customer-centred business, and they’re looking after their customers, I think it’s going to be a really positive year.”