Have a look at the good and bad sides of commission and the brokers who are taking a different approach

The commission structure of the mortgage industry has been interrogated from all sides in recent months, triggered by certain comments from the RBA.

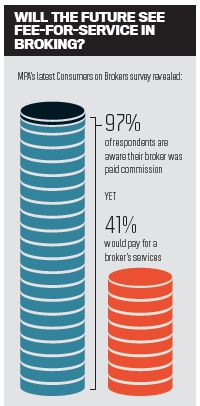

The mortgage industry has had to defend itself against a domino effect of scrutiny into its commission-based structure earlier this year, leading to the Mortgage and Finance Association of Australia (MFAA) and Finance Brokers Association of Australia (FBAA) rallying to the commission cause.

Shortly after the Reserve Bank of Australia inferred that the growing mortgage industry could fuel risks to the financial system, a review of the life insurance sector led to a call by some for commissions to be phased out and speculation that the same might happen within the mortgage broker sphere.

With all the discussion surrounding commissions, does it really remain the most effective model for brokers? What are its pros and cons, and who are those doing just fine without it?

MPA heard what the industry’s associations and franchise Mortgage Choice had to say on the subject and caught up with two brokerages that are thriving on a less traditional ‘hybrid’ model.

Commission-only pros and cons

Commission-based pay has its benefits, with flexibility and uncapped earning potential at the top of the list. But this brings with it less security than that offered by a salaried position and takes time to get a sure footing when starting out.

Franchise giant Mortgage Choice is well aware of the draws associated with a commission-only model but that the cons must be considered too.

“Most notably, the property market is cyclical – sometimes it is hot and other times it is not,” says CEO Michael Russell. “And, at times when it is not hot, brokers operating on a commission-only model may find it hard to generate a good income.”

Russell says this is true especially for newcomers to the industry. “Because of the way commissions are paid (once the loan settles) it can take quite a while for brokers (especially new entrants) to earn money,” he says.

Ren Wong, managing director of multiaward winning Sydney-based brokerage N1 Finance, also sees the toll that the first few months can take on new brokers. “The downside is that commission-only models deter young brokers entering the industry as it can take up to six months to generate a decent level of income,” says Wong.

“As a result, mortgage firms risk losing new entrants, making it difficult to recruit and expand.” But the uncapped earning potentialof commission-pay is a major benefit in being a finance broker and for brokerages, says FBAA CEO Peter White. “If you’re going to drive a sales team, and you put a cap on their earning potential, then they’re not going to perform that well or they’re going to get to a certain level and not perform any further.”

Similarly, Mortgage Choice’s Russell says that the commission factor is a huge motivator in the industry, keeping brokers looking for ways to bring business through the door. “It forces mortgage brokers to work hard and be constantly undertaking high- net-worth activities. Furthermore, it forces them to take a savvy approach to business.”

And although he notes the downside of commission, Wong sees the plus-side of uncapped potential while benefiting a firm with lower fixed costs.

A hybrid model tried and tested

A hybrid model tried and tested

With so many factors pulling commissions in opposite directions, some brokerages have taken the choicest aspects of salary and commission to create the most effective situation for their brokers.

Canberra’s top brokerage, Tiffen & Co, second on MPA’s Top 10 Independent Brokerages of 2014 and operating in its 21st year, knows what works and what doesn’t. Managing director Gerard Tiffen runs his brokerage on a part-salary/partcommission model, offering brokers salary and commission, based on settlement hurdles. Tiffen says that from an owner’s perspective, the commission-only model is appealing as their income will reflect their performance. “However, I think a mix is the best model as it gives you a base to work from, yet still incentivises you to take the best care possible of every client and grow your network.”

N1 Finance has also steered away from commission-only pay, offering their brokers the stability that salary brings but with a bonus component for upside earning potential. “Salary-based compensation also has its own drawbacks, as it can remove the reward for ambitious employees to go beyond their basic job description,” says Wong.

“This ‘hybrid’ model offers a base salary plus commission or bonus for high performance. So although the risk is less as a broker can rely on a guaranteed salary, the rewards are also less than an un-capped commission-only model.”

Wong says this model has been a perfect fit for N1 Finance, attracting brokers committed to a long-term broking career. “It allows our employees to focus on training and completing tasks properly without worrying about writing loans to pay for day-to-day expenses.”

As a franchise, Mortgage Choice says only their franchisees work off a commission-only model, since their self-employed status allows them to choose how they wish to be paid. “All of our full-time loan writers (excluding franchisees) are entitled to be paid a salary,” says Russell. “Many of (our) loan writers work under a part-salary/part-commission or bonus incentive model, whereby their franchisee/business manager pays them a salary as well as a bonus or commission based on the level of business they write.”

“Loan writers are considered a level 4 under the Banking Finance and Insurance Award, and the minimum base for an adult level 4 is currently $43,035.” He says if it’s expected that staff will work back, their managers will need to pay them overtime, penalties and shift allowances.

And the MFAA notes that some brokerages offer salaried options for new recruits. “Aussie initially led the industry by offering a salaried model for new entrants,” says MFAA CEO Siobhan Hayden. “But brokerages around the country are now offering a salaried or retainer initially whilst the broker establishes their business.”

But there have been a number of models in the industry for a long time, says FBAA’s White.“The reality is with most brokerages or aggregation firms, they’re running on the premise of you’re a commission-only broker. It depends how each aggregator has modelled themselves and none of them are right, and none of them are wrong. It’s all a commercial positioning that they choose to undertake that best suits them for whatever reason that is.”

Although White doesn’t believe there will be an increase in the hybrid model in the future, if there was hypothetically, “it would be less competitive, because people aren’t trying to clamber over every deal”.

A future where commissions take a step back?

If commissions weren’t centre stage, would it change the face of the industry?

“I think it would definitely change the landscape,” says Tiffen. “I think there would be a lot more consolidation between industries – accountants, financial planners and mortgage brokers, if this was the case.”

“In a mature environment, it is common for businesses within the industry to consolidate,” the MFAA’s Hayden says. “We are already seeing this within our industry and with consolidation, businesses are better positioned to provide salaried models for recruitment.”

Wong says the industry would probably morph into a likeness of the bank model, where brokers are paid a base salary and set a target to reach for potential bonuses.

Mortgage Choice’s Russell expects to see more combined models in the future as the benefits offered become more widespread. “We wouldn’t be surprised to see an increasing number of other aggregators and business owners paying their loan writer staff a salary as well as certain commission/bonus incentives.”

The mortgage industry has had to defend itself against a domino effect of scrutiny into its commission-based structure earlier this year, leading to the Mortgage and Finance Association of Australia (MFAA) and Finance Brokers Association of Australia (FBAA) rallying to the commission cause.

Shortly after the Reserve Bank of Australia inferred that the growing mortgage industry could fuel risks to the financial system, a review of the life insurance sector led to a call by some for commissions to be phased out and speculation that the same might happen within the mortgage broker sphere.

With all the discussion surrounding commissions, does it really remain the most effective model for brokers? What are its pros and cons, and who are those doing just fine without it?

MPA heard what the industry’s associations and franchise Mortgage Choice had to say on the subject and caught up with two brokerages that are thriving on a less traditional ‘hybrid’ model.

Commission-only pros and cons

Commission-based pay has its benefits, with flexibility and uncapped earning potential at the top of the list. But this brings with it less security than that offered by a salaried position and takes time to get a sure footing when starting out.

Franchise giant Mortgage Choice is well aware of the draws associated with a commission-only model but that the cons must be considered too.

“Most notably, the property market is cyclical – sometimes it is hot and other times it is not,” says CEO Michael Russell. “And, at times when it is not hot, brokers operating on a commission-only model may find it hard to generate a good income.”

Russell says this is true especially for newcomers to the industry. “Because of the way commissions are paid (once the loan settles) it can take quite a while for brokers (especially new entrants) to earn money,” he says.

Ren Wong, managing director of multiaward winning Sydney-based brokerage N1 Finance, also sees the toll that the first few months can take on new brokers. “The downside is that commission-only models deter young brokers entering the industry as it can take up to six months to generate a decent level of income,” says Wong.

“As a result, mortgage firms risk losing new entrants, making it difficult to recruit and expand.” But the uncapped earning potentialof commission-pay is a major benefit in being a finance broker and for brokerages, says FBAA CEO Peter White. “If you’re going to drive a sales team, and you put a cap on their earning potential, then they’re not going to perform that well or they’re going to get to a certain level and not perform any further.”

Similarly, Mortgage Choice’s Russell says that the commission factor is a huge motivator in the industry, keeping brokers looking for ways to bring business through the door. “It forces mortgage brokers to work hard and be constantly undertaking high- net-worth activities. Furthermore, it forces them to take a savvy approach to business.”

And although he notes the downside of commission, Wong sees the plus-side of uncapped potential while benefiting a firm with lower fixed costs.

A hybrid model tried and testedWith so many factors pulling commissions in opposite directions, some brokerages have taken the choicest aspects of salary and commission to create the most effective situation for their brokers.

Canberra’s top brokerage, Tiffen & Co, second on MPA’s Top 10 Independent Brokerages of 2014 and operating in its 21st year, knows what works and what doesn’t. Managing director Gerard Tiffen runs his brokerage on a part-salary/partcommission model, offering brokers salary and commission, based on settlement hurdles. Tiffen says that from an owner’s perspective, the commission-only model is appealing as their income will reflect their performance. “However, I think a mix is the best model as it gives you a base to work from, yet still incentivises you to take the best care possible of every client and grow your network.”

N1 Finance has also steered away from commission-only pay, offering their brokers the stability that salary brings but with a bonus component for upside earning potential. “Salary-based compensation also has its own drawbacks, as it can remove the reward for ambitious employees to go beyond their basic job description,” says Wong.

“This ‘hybrid’ model offers a base salary plus commission or bonus for high performance. So although the risk is less as a broker can rely on a guaranteed salary, the rewards are also less than an un-capped commission-only model.”

Wong says this model has been a perfect fit for N1 Finance, attracting brokers committed to a long-term broking career. “It allows our employees to focus on training and completing tasks properly without worrying about writing loans to pay for day-to-day expenses.”

As a franchise, Mortgage Choice says only their franchisees work off a commission-only model, since their self-employed status allows them to choose how they wish to be paid. “All of our full-time loan writers (excluding franchisees) are entitled to be paid a salary,” says Russell. “Many of (our) loan writers work under a part-salary/part-commission or bonus incentive model, whereby their franchisee/business manager pays them a salary as well as a bonus or commission based on the level of business they write.”

“Loan writers are considered a level 4 under the Banking Finance and Insurance Award, and the minimum base for an adult level 4 is currently $43,035.” He says if it’s expected that staff will work back, their managers will need to pay them overtime, penalties and shift allowances.

And the MFAA notes that some brokerages offer salaried options for new recruits. “Aussie initially led the industry by offering a salaried model for new entrants,” says MFAA CEO Siobhan Hayden. “But brokerages around the country are now offering a salaried or retainer initially whilst the broker establishes their business.”

But there have been a number of models in the industry for a long time, says FBAA’s White.“The reality is with most brokerages or aggregation firms, they’re running on the premise of you’re a commission-only broker. It depends how each aggregator has modelled themselves and none of them are right, and none of them are wrong. It’s all a commercial positioning that they choose to undertake that best suits them for whatever reason that is.”

Although White doesn’t believe there will be an increase in the hybrid model in the future, if there was hypothetically, “it would be less competitive, because people aren’t trying to clamber over every deal”.

A future where commissions take a step back?

If commissions weren’t centre stage, would it change the face of the industry?

“I think it would definitely change the landscape,” says Tiffen. “I think there would be a lot more consolidation between industries – accountants, financial planners and mortgage brokers, if this was the case.”

“In a mature environment, it is common for businesses within the industry to consolidate,” the MFAA’s Hayden says. “We are already seeing this within our industry and with consolidation, businesses are better positioned to provide salaried models for recruitment.”

Wong says the industry would probably morph into a likeness of the bank model, where brokers are paid a base salary and set a target to reach for potential bonuses.

Mortgage Choice’s Russell expects to see more combined models in the future as the benefits offered become more widespread. “We wouldn’t be surprised to see an increasing number of other aggregators and business owners paying their loan writer staff a salary as well as certain commission/bonus incentives.”